Steel Decarbonization Market Revenue, Trends, and Strategic Insights by 2035

Steel Decarbonization Market Size

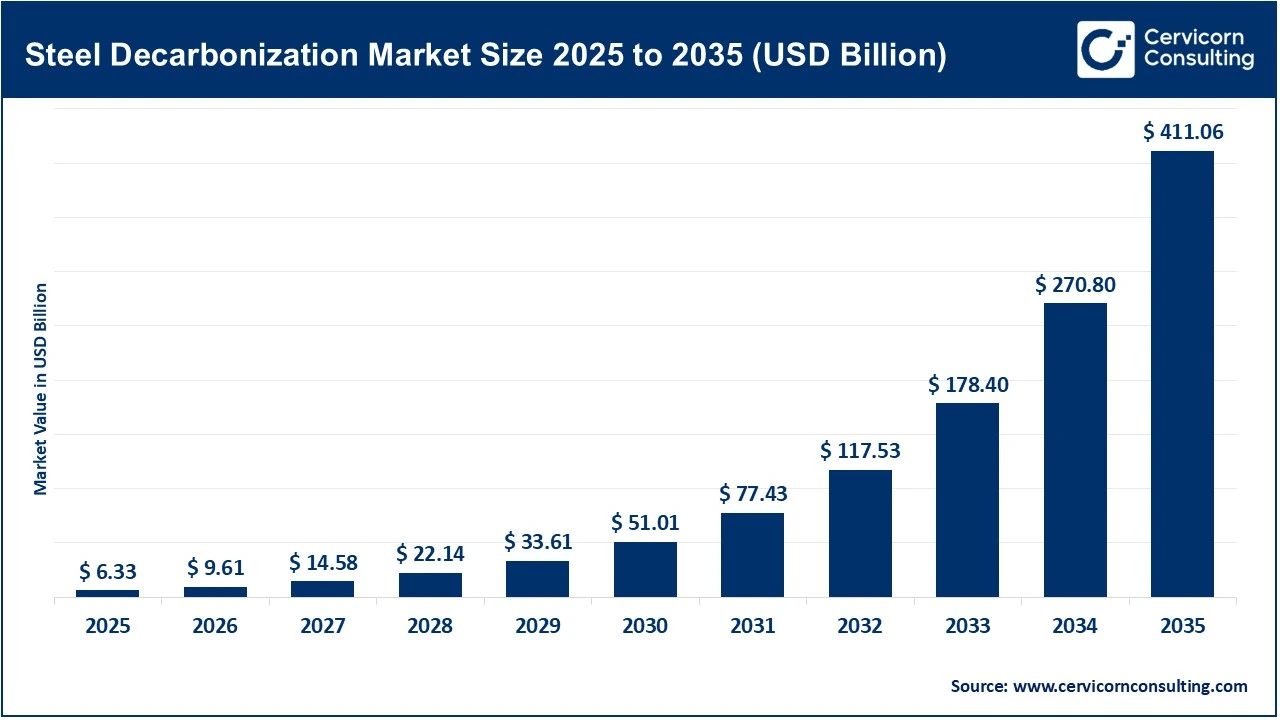

The global steel decarbonization market was estimated at about USD 6.33 billion in 2025 and is projected to reach nearly USD 411.06 billion by 2035, expanding at a CAGR of 51.88%.

What is the Steel Decarbonization Market?

The steel decarbonization market refers to the global ecosystem of technologies, investments, infrastructure, and policies aimed at reducing or eliminating carbon emissions from steel manufacturing processes. Traditionally, steel has been produced using coal-based blast furnaces, which are highly carbon-intensive. Decarbonization replaces or modifies these processes with cleaner alternatives such as hydrogen-based reduction, scrap-based electric arc furnaces, renewable-powered production systems, and carbon capture technologies. The market includes both greenfield projects (new green steel plants) and brownfield retrofits (upgrading existing steel facilities). According to industry analysis, steel decarbonization is essential because steel production is one of the largest industrial emitters globally, making its transition crucial for achieving net-zero climate targets.

Why is it Important?

Steel decarbonization is important for three interconnected reasons: environmental necessity, regulatory pressure, and industrial competitiveness. Environmentally, the steel sector is one of the highest contributors to greenhouse gas emissions, and reducing these emissions is critical to meeting global climate goals such as the Paris Agreement. Economically, governments across Europe, North America, and Asia are implementing carbon pricing systems, emissions trading schemes, and border adjustment mechanisms that make high-carbon steel increasingly expensive. Strategically, industries such as automotive, construction, and renewable energy are demanding low-carbon steel to decarbonize their own supply chains. This creates a strong downstream market pull for green steel. Additionally, companies that adopt early decarbonization strategies are gaining long-term competitive advantages through access to premium markets, subsidies, and green financing instruments.

Steel Decarbonization Market Growth Factors

The growth of the steel decarbonization market is driven by a combination of regulatory mandates, technological advancements, rising demand for sustainable materials, and large-scale public-private investments; stringent global climate policies such as carbon pricing, EU Green Deal frameworks, and the U.S. Inflation Reduction Act are accelerating the transition toward low-emission steel production, while rapid advancements in hydrogen-based direct reduced iron (H2-DRI), electric arc furnace (EAF) efficiency, and carbon capture technologies are making decarbonized steel economically viable over time; simultaneously, increasing demand from automotive manufacturers, construction companies, and infrastructure developers for low-carbon materials is creating strong downstream pressure, and significant investments from governments and steelmakers into renewable energy integration, green hydrogen production, and circular economy models based on scrap recycling are further reinforcing long-term market expansion and scalability.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2934

Key Companies in the Steel Decarbonization Market

1. ArcelorMittal

- Specialization: Integrated steel production transitioning to hydrogen-based steelmaking and carbon-neutral operations

- Key Focus Areas: Hydrogen DRI projects, EAF expansion, CCUS pilots, XCarb low-carbon steel brand

- Notable Features: Global leader in steel production with strong decarbonization roadmap

- 2024 Revenue: ~USD 68–70 billion (steel segment dependent, estimated range based on recent filings)

- Market Share: One of the top 3 global steel producers

- Global Presence: Operations across Europe, Americas, Asia, and Africa

ArcelorMittal is actively investing in hydrogen-ready furnaces and low-carbon steel supply chains but faces challenges due to high capital costs and policy uncertainty.

2. Nucor Corporation

- Specialization: Electric arc furnace (EAF)-based steel production using recycled scrap

- Key Focus Areas: Scrap recycling, renewable energy integration, low-emission steel manufacturing

- Notable Features: One of the most energy-efficient steelmakers in North America

- 2024 Revenue: ~USD 30–35 billion (approx.)

- Market Share: Leading U.S. steel producer

- Global Presence: Primarily United States with expanding international influence

Nucor’s decarbonization advantage lies in its scrap-based EAF model, which already produces significantly lower emissions than traditional blast furnaces.

3. POSCO

- Specialization: Integrated steel production with hydrogen reduction research

- Key Focus Areas: Hydrogen ironmaking, carbon neutrality by 2050, smart steel plants

- Notable Features: Strong R&D investments in green steel technologies

- 2024 Revenue: ~USD 60–65 billion (estimated)

- Market Share: Major global steel producer, especially in Asia

- Global Presence: South Korea, India, Vietnam, global subsidiaries

POSCO is transitioning from coal-heavy production toward hydrogen-based steelmaking and is building large-scale green steel infrastructure.

4. Thyssenkrupp Steel Europe

- Specialization: Integrated steel production with hydrogen-based transformation

- Key Focus Areas: tkH2Steel project, hydrogen DRI plants, emission reduction programs

- Notable Features: One of Europe’s most ambitious industrial decarbonization programs

- 2024 Revenue: ~USD 15–20 billion (steel division estimate)

- Market Share: Key European steel producer

- Global Presence: Primarily Europe

The company is heavily supported by EU subsidies for hydrogen steel transformation but faces cost pressures and delayed investments.

5. SSAB

- Specialization: Fossil-free steel using hydrogen-based HYBRIT technology

- Key Focus Areas: Hydrogen DRI, fossil-free steel supply chain, automotive partnerships

- Notable Features: First company to deliver fossil-free steel commercially

- 2024 Revenue: ~USD 10–12 billion (estimated)

- Market Share: Niche leader in premium green steel

- Global Presence: Sweden, Finland, Europe, expanding exports

SSAB is a pioneer in green steel and has already demonstrated commercial viability of hydrogen-based steel production.

Leading Trends and Their Impact

One of the most significant trends in the steel decarbonization market is the rapid shift toward hydrogen-based direct reduction iron (H2-DRI) systems, which eliminate coal from the steelmaking process and replace it with green hydrogen, significantly reducing CO₂ emissions. Another key trend is the expansion of electric arc furnace (EAF) technology, which uses scrap steel and renewable electricity, making it one of the most scalable low-carbon solutions. Carbon capture, utilization, and storage (CCUS) is also gaining traction as a transitional solution for existing blast furnaces. Additionally, circular economy models focusing on scrap recycling are reshaping raw material sourcing. These trends are collectively driving long-term cost reductions, improving sustainability performance, and creating new investment opportunities across the steel value chain.

Successful Examples of Steel Decarbonization Worldwide

Several real-world projects demonstrate the viability of steel decarbonization. SSAB’s fossil-free steel delivery to automotive manufacturers marked a global milestone in hydrogen-based steel production. In Sweden, HYBRIT (a collaboration between SSAB, LKAB, and Vattenfall) has pioneered hydrogen reduction technology at scale. In Europe, ArcelorMittal has launched multiple pilot hydrogen DRI projects under its XCarb initiative. In North America, Nucor continues to expand low-emission EAF capacity powered by renewable energy. Meanwhile, startups such as Boston Metal are advancing molten oxide electrolysis technology, which could potentially revolutionize steel production by eliminating carbon entirely. These examples highlight that decarbonized steel is no longer theoretical but increasingly commercially viable.

Global Regional Analysis, Government Initiatives, and Policies

Europe

Europe is the global leader in steel decarbonization, driven by the EU Green Deal, carbon border adjustment mechanism (CBAM), and strong subsidy programs supporting hydrogen infrastructure. Countries like Germany and Sweden are investing heavily in hydrogen-based steel projects, though high energy costs and economic pressures are slowing implementation.

North America

The United States is accelerating decarbonization through policies like the Inflation Reduction Act (IRA), which provides tax incentives for clean hydrogen and renewable energy integration. Companies like Nucor are expanding EAF capacity, supported by abundant scrap supply and relatively flexible regulatory frameworks.

Asia-Pacific

Asia-Pacific, led by China, Japan, and South Korea, is rapidly scaling green steel initiatives. Governments are investing in carbon neutrality roadmaps, renewable energy expansion, and hydrogen infrastructure. POSCO and other regional giants are leading hydrogen steel R&D efforts.

Middle East & Emerging Regions

Countries such as the UAE and Saudi Arabia are exploring green hydrogen-based industrial hubs, positioning themselves as future exporters of low-carbon steel due to access to cheap renewable energy.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Specialty Gas Market Revenue, Trends, and Strategic Insights by 2035