3D Printing in Defence Market Revenue, Trends, and Strategic Insights by 2035

3D Printing in Defence Market Size

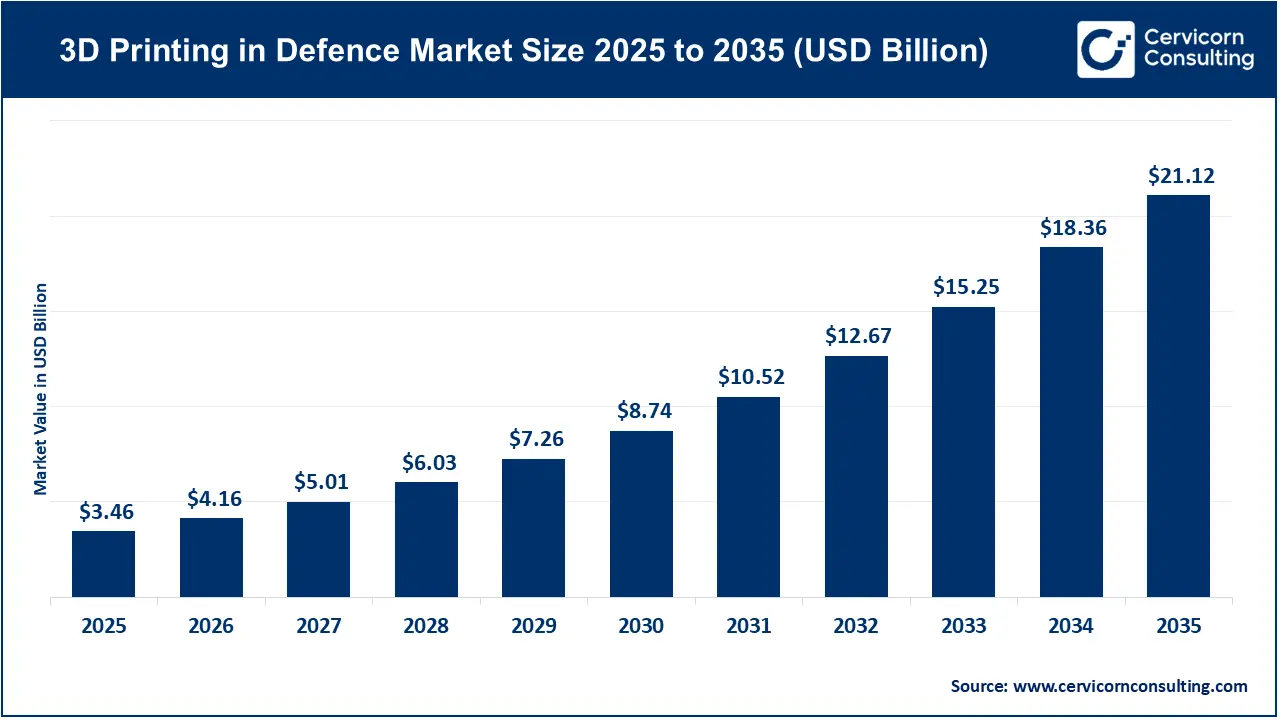

The global 3D printing in defence market was valued at approximately USD 3.46 billion in 2025 and is projected to reach nearly USD 21.12 billion by 2035, growing at a CAGR of 19.83%.

What is the 3D Printing in Defence Market?

The 3D printing in defence market refers to the ecosystem of technologies, materials, software, equipment, and services used to manufacture military components and systems through additive manufacturing processes. Unlike traditional manufacturing methods that remove material through cutting or machining, 3D printing builds objects layer by layer using digital models.

Defense organizations utilize 3D printing to manufacture:

- Aircraft and spacecraft components

- Weapon system parts

- Military vehicle components

- Naval equipment

- Drones and unmanned systems

- Tactical gear and protective equipment

- Medical devices for military healthcare

- Maintenance and replacement parts

The technology encompasses various additive manufacturing techniques including:

- Selective Laser Melting (SLM)

- Direct Metal Laser Sintering (DMLS)

- Fused Deposition Modeling (FDM)

- Stereolithography (SLA)

- Electron Beam Melting (EBM)

- Binder Jetting

These technologies enable defense manufacturers to produce highly complex geometries that would be difficult or impossible using conventional manufacturing processes.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2670

Why is 3D Printing Important in Defence?

Enhanced Military Readiness

One of the most significant advantages of additive manufacturing is its ability to produce critical replacement parts quickly. Military forces often operate in remote locations where logistics support can be challenging. 3D printing enables on-demand production of essential components, reducing equipment downtime.

Supply Chain Resilience

Global geopolitical tensions and supply chain disruptions have highlighted vulnerabilities in traditional manufacturing systems. Defense organizations are increasingly using additive manufacturing to localize production and reduce dependence on external suppliers.

Reduced Manufacturing Costs

Complex military components often require multiple manufacturing steps. 3D printing consolidates these processes, reducing labor, tooling requirements, and material waste.

Lightweight Military Systems

Weight reduction is crucial in aerospace and defense applications. Additive manufacturing allows engineers to design lightweight structures while maintaining strength and durability.

Rapid Prototyping and Innovation

Military research programs benefit significantly from faster prototyping cycles. Engineers can design, test, and modify components rapidly, accelerating defense innovation.

Battlefield Manufacturing

Advanced portable 3D printing systems are enabling military units to manufacture parts directly in operational environments, reducing dependency on centralized supply chains.

Major Companies Shaping the 3D Printing in Defence Market

| Company | Specialization | Key Focus Areas | Notable Features | 2025 Revenue* | Market Share* | Global Presence |

|---|---|---|---|---|---|---|

| Lockheed Martin Corporation | Defense systems and aerospace manufacturing | Aerospace components, missiles, satellites, military aircraft | Extensive use of additive manufacturing in advanced defense programs | Multi-billion USD defense revenue | Significant defense AM user | North America, Europe, Asia-Pacific, Middle East |

| 3D Systems Corporation | Industrial 3D printing solutions | Metal and polymer additive manufacturing | Aerospace-grade certified manufacturing technologies | Hundreds of millions USD | Major AM technology provider | More than 20 countries |

| Desktop Metal, Inc. | Metal additive manufacturing | High-speed metal printing for defense and aerospace | Mass production capability for complex metal parts | Growing industrial manufacturing revenue | Emerging market leader | North America, Europe, Asia |

| SLM Solutions Group AG | Metal additive manufacturing systems | Selective laser melting technology | Large-scale metal component production | Strong industrial AM revenues | Leading metal AM supplier | Europe, North America, Asia-Pacific |

| Stratasys Ltd. | Polymer-based additive manufacturing | Military prototyping and production systems | Advanced FDM and PolyJet technologies | Over USD 600 million range | Global AM leader | Worldwide operations across major defense markets |

*Revenue and market share figures vary based on reporting periods and business segments.

Leading Trends in the 3D Printing in Defence Market and Their Impact

Expansion of Metal Additive Manufacturing

Metal additive manufacturing has become one of the most important trends in the defense sector. Military applications require durable, heat-resistant, and high-strength components capable of operating under extreme conditions.

Impact

- Improved performance of aircraft engines

- Stronger missile components

- Enhanced durability of military vehicles

- Reduced production timelines

Adoption of Digital Inventory Systems

Defense agencies are increasingly moving toward digital inventories where component designs are stored electronically and manufactured when required.

Impact

- Reduced warehouse costs

- Faster replacement part availability

- Improved operational readiness

- Lower logistics expenses

Integration with Artificial Intelligence

AI-driven design optimization is helping defense manufacturers create components with superior strength-to-weight ratios.

Impact

- More efficient military systems

- Enhanced structural integrity

- Lower material consumption

- Faster design validation

Portable Battlefield Manufacturing

Military organizations are deploying mobile additive manufacturing units capable of operating in combat zones and remote military bases.

Impact

- Reduced supply chain dependency

- Faster maintenance operations

- Improved mission success rates

- Enhanced operational flexibility

Advanced Materials Development

Research is accelerating in military-grade materials including titanium alloys, nickel superalloys, advanced polymers, and composite materials.

Impact

- Better thermal resistance

- Improved component lifespan

- Greater mission reliability

- Enhanced weapon system performance

Additive Manufacturing for Unmanned Systems

Drones and autonomous defense platforms increasingly rely on 3D printed components.

Impact

- Rapid development cycles

- Lower production costs

- Greater customization capabilities

- Improved deployment speed

Successful Examples of 3D Printing in Defence Around the World

United States Air Force

The U.S. Air Force has extensively integrated additive manufacturing into aircraft maintenance programs. Critical replacement parts for aging aircraft are now being produced using advanced metal 3D printing technologies.

Results

- Reduced maintenance downtime

- Extended aircraft lifespan

- Lower procurement costs

U.S. Navy Shipboard Manufacturing

The U.S. Navy has deployed additive manufacturing systems aboard ships to produce replacement components while at sea.

Results

- Reduced logistical delays

- Increased mission readiness

- Improved operational independence

Lockheed Martin’s Satellite Components

Lockheed Martin utilizes additive manufacturing for satellite structures and aerospace systems.

Results

- Significant weight reduction

- Improved performance

- Reduced production complexity

British Army Additive Manufacturing Initiative

The United Kingdom Ministry of Defence is exploring battlefield 3D printing to support deployed forces.

Results

- Rapid spare-part production

- Reduced inventory requirements

- Enhanced operational efficiency

Australian Defence Force Programs

Australia is investing heavily in additive manufacturing technologies for aerospace and naval applications.

Results

- Strengthened domestic manufacturing

- Improved defense self-reliance

- Enhanced supply chain resilience

European Defence Additive Manufacturing Projects

Several NATO member countries are collaborating on additive manufacturing initiatives aimed at standardizing military production capabilities.

Results

- Increased interoperability

- Shared manufacturing resources

- Improved military logistics

Global Regional Analysis of the 3D Printing in Defence Market

North America

North America represents the largest market for defense-related additive manufacturing due to substantial defense spending, technological leadership, and strong aerospace manufacturing capabilities.

Key Growth Drivers

- High military budgets

- Strong defense contractor ecosystem

- Extensive R&D investments

- Rapid adoption of advanced manufacturing technologies

Government Initiatives and Policies

The United States Department of Defense actively supports additive manufacturing through modernization programs, innovation grants, and research partnerships with defense contractors and universities.

Programs focus on:

- Military supply chain modernization

- Advanced manufacturing innovation

- Aerospace component production

- Battlefield manufacturing capabilities

Canada is also investing in advanced manufacturing technologies to strengthen defense industrial capabilities and improve domestic production.

Europe

Europe is emerging as a major hub for defense additive manufacturing due to growing defense expenditures, increasing geopolitical concerns, and strong industrial capabilities.

Key Growth Drivers

- Expansion of military modernization programs

- NATO capability development initiatives

- Advanced aerospace manufacturing infrastructure

- Government support for Industry 4.0 technologies

Government Initiatives and Policies

The European Union is encouraging collaborative defense manufacturing projects through funding mechanisms and industrial partnerships.

Several countries including:

- Germany

- France

- United Kingdom

- Italy

- Netherlands

are investing heavily in additive manufacturing research for defense applications.

Defense ministries are supporting:

- Digital manufacturing programs

- Military innovation centers

- Aerospace additive manufacturing projects

- Defense technology accelerators

Germany’s advanced industrial base and leadership in metal additive manufacturing continue to support regional market growth.

Asia-Pacific

Asia-Pacific is expected to experience the fastest growth in the 3D printing in defence market due to increasing military spending, territorial security concerns, and expanding indigenous defense manufacturing initiatives.

Key Growth Drivers

- Rising defense budgets

- Indigenous military production programs

- Rapid technological advancements

- Growing aerospace manufacturing sectors

Government Initiatives and Policies

China

China has incorporated additive manufacturing into national defense modernization strategies.

Key focus areas include:

- Military aerospace systems

- Advanced weapon platforms

- Naval applications

- Space defense technologies

India

India’s “Make in India” initiative is promoting domestic defense manufacturing, including additive manufacturing adoption.

Government priorities include:

- Defense self-reliance

- Localized military production

- Advanced manufacturing capabilities

- Indigenous aerospace development

Japan

Japan is investing in advanced manufacturing technologies to enhance defense readiness and strengthen domestic production capabilities.

South Korea

South Korea is integrating additive manufacturing into military modernization programs, particularly in aerospace and naval sectors.

Regional Outlook

Asia-Pacific is becoming a strategic manufacturing center for military technologies, supported by government investments and increasing defense innovation activities.

Latin America

The Latin American market remains relatively smaller but is gradually adopting additive manufacturing technologies for defense modernization.

Key Growth Drivers

- Military equipment modernization

- Aerospace industry growth

- Cost-effective manufacturing requirements

Government Initiatives and Policies

Countries such as Brazil are investing in aerospace manufacturing and defense technology development.

Government programs focus on:

- Domestic defense production

- Aerospace innovation

- Technology transfer initiatives

Brazil’s strong aerospace sector provides a foundation for future growth in defense additive manufacturing applications.

Middle East and Africa

The Middle East and Africa region is increasingly exploring additive manufacturing technologies to strengthen defense capabilities and reduce import dependence.

Key Growth Drivers

- Rising defense expenditures

- Military modernization initiatives

- Strategic self-sufficiency goals

- Expansion of domestic manufacturing capabilities

Government Initiatives and Policies

United Arab Emirates

The UAE has launched national strategies supporting advanced manufacturing and Industry 4.0 adoption.

Defense-related objectives include:

- Local manufacturing expansion

- Technology innovation

- Military logistics optimization

Saudi Arabia

Saudi Arabia’s Vision 2030 program promotes localization of defense manufacturing and advanced industrial technologies.

Key priorities include:

- Defense industrial development

- Technology transfer

- Local content enhancement

- Advanced manufacturing investments

South Africa

South Africa continues to leverage its established defense industry and aerospace expertise to explore additive manufacturing opportunities.

Regional Outlook

Growing emphasis on military self-reliance and industrial diversification is expected to accelerate adoption of additive manufacturing technologies throughout the Middle East and Africa.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Video Games Market Revenue, Trends, and Strategic Insights by 2035