Silicon Photonics Market Revenue, Trends, and Regional Forecasts by 2034

Silicon Photonics Market Size

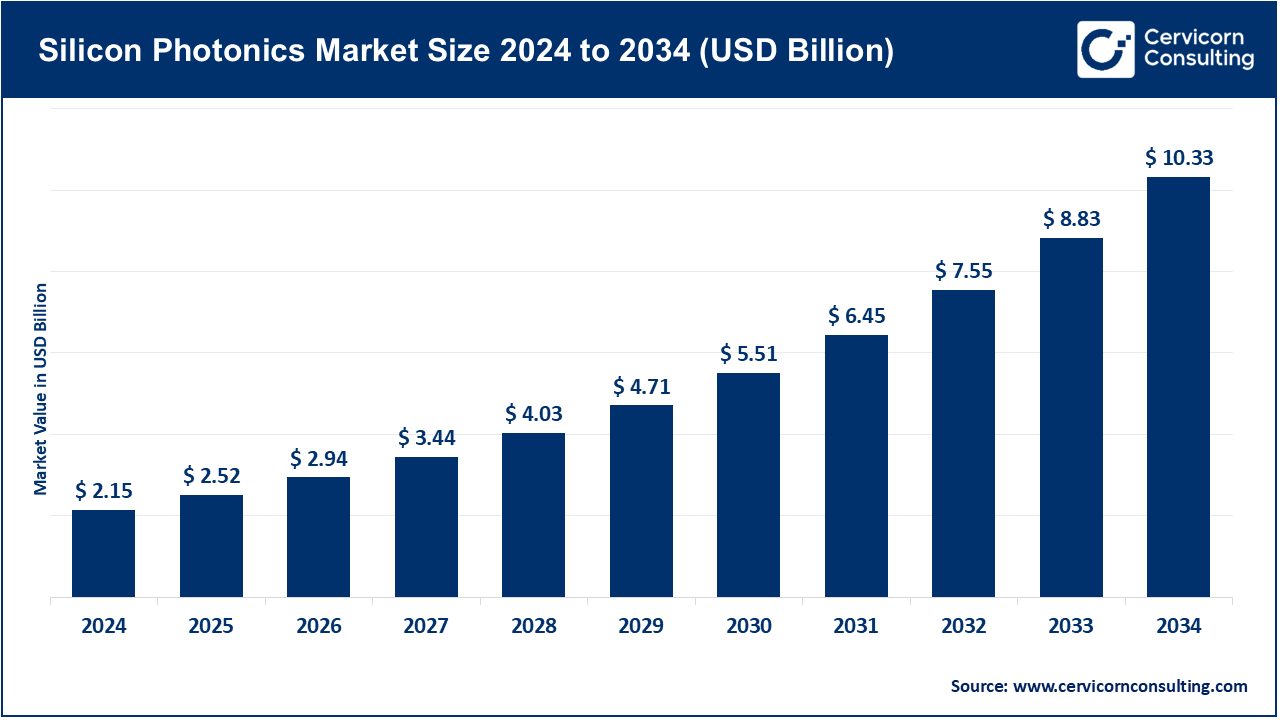

The global silicon photonics market size was worth USD 2.15 billion in 2024 and is anticipated to expand to around USD 10.33 billion by 2034, registering a compound annual growth rate (CAGR) of 26.32% from 2025 to 2034.

What Is the Silicon Photonics Market?

Silicon photonics refers to the integration of optical devices such as lasers, modulators, and detectors onto silicon chips to enable high-speed data transfer using light rather than electrical signals. This transformative technology combines the cost-effectiveness and scale of silicon semiconductor manufacturing with the ultra-fast transmission capabilities of photonics. The market encompasses a range of components and systems used in data centers, telecommunications, high-performance computing (HPC), biosensing, quantum computing, and autonomous vehicle lidar.

In 2024, the silicon photonics market is valued between USD 1.6 billion to USD 3.3 billion depending on the scope of analysis, with forecasts estimating the market could reach between USD 8 billion and USD 15 billion by 2030. This rapid growth is driven by increasing bandwidth needs, energy efficiency imperatives, and strategic interest from national governments investing in photonics innovation.

Growth Factors

The rapid expansion of the silicon photonics market is primarily fueled by the surging demand for high-bandwidth data transmission in data centers, the exponential growth in artificial intelligence and machine learning workloads, and the deployment of 5G infrastructure requiring advanced backhaul and fronthaul networks. Other key drivers include the increasing need for energy-efficient computing systems, miniaturization of optical components, and the rise of autonomous vehicles utilizing lidar systems. Significant government initiatives, such as the U.S. CHIPS and Science Act and Europe’s multi-billion-euro investments in photonics pilot lines, are injecting momentum into domestic photonic manufacturing ecosystems. Additionally, technological advances like 300 mm wafer processing, co-packaged optics, and mature CMOS-photonics integration are enabling cost-effective and scalable production of photonics devices.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2682

Why Is It Important?

Silicon photonics is emerging as a cornerstone technology for the next generation of data-centric infrastructure. The importance lies in its ability to drastically improve data transmission rates while reducing power consumption and physical footprint. For instance, where traditional copper-based interconnects face bandwidth and heat dissipation limitations, silicon photonics offers multi-terabit per second transmission with lower latency and improved energy efficiency. These advantages are crucial in scaling data centers for AI applications, enabling faster telecom networks, supporting real-time data processing in autonomous vehicles, and advancing scientific research through quantum communications and biosensing. Moreover, photonic components can be fabricated using existing semiconductor manufacturing infrastructure, enhancing their commercial viability and accelerating global adoption.

Top Companies: Overview & Profiles

Intel Corporation

- Specialization: High-performance silicon photonics transceivers and optical I/O chips.

- Key Focus Areas: Data center interconnects, co-packaged optics, and integrated optical networking solutions.

- Notable Features: Developed 400G and 800G optical modules, pioneering 1.6 Tbps optical interconnects.

- 2024 Revenue / Market Share: Estimated to hold 30–40% of the silicon photonics transceiver market.

- Global Presence: North America-based with global customer deployment.

Cisco Systems, Inc.

- Specialization: Integration of photonic modules into network switches and routers.

- Key Focus Areas: Enterprise networking, 5G infrastructure, and high-speed telecom backbones.

- Notable Features: Deploys high-bandwidth optical transceivers embedded in network equipment.

- 2024 Revenue / Market Share: Among top five global players.

- Global Presence: Sales and R&D in Americas, Europe, and Asia-Pacific.

DAS Photonics

- Specialization: Custom photonic integrated circuits (PICs) and modules.

- Key Focus Areas: Signal processing, aerospace technologies, and optical communications.

- Notable Features: European innovator offering application-specific photonic solutions.

- 2024 Revenue / Market Share: Niche player recognized among top 2024 vendors.

- Global Presence: Headquartered in Spain, active in EU and North America.

Hamamatsu Photonics K.K.

- Specialization: Optical detectors, sensors, and advanced photonic devices.

- Key Focus Areas: Biosensing, diagnostics, and scientific instrumentation.

- Notable Features: High-precision components for industrial and research sectors.

- 2024 Revenue / Market Share: Among top ten component manufacturers.

- Global Presence: Headquartered in Japan, global manufacturing and sales.

IBM Corporation

- Specialization: R&D in integrated silicon photonics for AI and HPC.

- Key Focus Areas: Quantum computing, optical packaging, and system integration.

- Notable Features: Strong focus on innovation and collaborative research.

- 2024 Revenue / Market Share: Leading in silicon photonics research and patents.

- Global Presence: Research labs and partnerships across global regions.

Leading Trends & Their Impact

- Co-Packaged Optics (CPO): Reduced energy use and increased bandwidth density by bringing optics closer to processing chips.

- Hyperscale Data Centers: Adoption of 800G and 1.6T optical modules driven by AI and cloud demands.

- AI/ML Workloads: Optical interconnects reduce bottlenecks in GPU-heavy infrastructure.

- 5G Telecom Growth: Advanced optical backhaul required for data-dense 5G applications.

- Automotive Lidar: Solid-state lidar systems powered by silicon photonics for autonomous navigation.

- Quantum Communications: Photonics chips for secure communication and quantum computing.

- National Photonics Initiatives: Governments boosting domestic capabilities to reduce foreign dependency.

Successful Global Examples

- NVIDIA DGX Systems: Uses silicon photonics for GPU interconnects in AI clusters.

- EU Photonics Pilot Lines: Funded facilities for photonic chip manufacturing in the Netherlands.

- GlobalFoundries NY: Building a silicon photonics-focused packaging center with federal support.

- Fudan University, China: Developed a 38 Tbps photonic chip for next-gen data centers.

- Taiwan AI Infrastructure: National AI projects incorporating photonic technologies with major industry backing.

Global Regional Analysis & Government Initiatives

North America

- Market Share: Holds ~35–38% of the global market.

- Key Programs: CHIPS and Science Act supports photonics manufacturing and R&D.

Europe

- Market Activity: Rapid growth through EU Chips Act and Photonics21.

- Investments: Over €100 million committed to pilot lines and fabs.

Asia-Pacific

- Growth Rate: Fastest-growing region with major investments in China, Taiwan, and India.

- Initiatives: National strategies to build domestic photonics supply chains.

Latin America, Middle East & Africa

- Market Maturity: Early-stage adoption with interest in biosensing and telecom.

- Government Support: Limited but growing through partnerships and imports.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Semiconductor Market Size, Growth Projections, Key Players, and Emerging Trends Shaping the Industry