Agrochemicals Market Growth Drivers, Trends, Key Players and Regional Insights by 2035

Agrochemicals Market Size

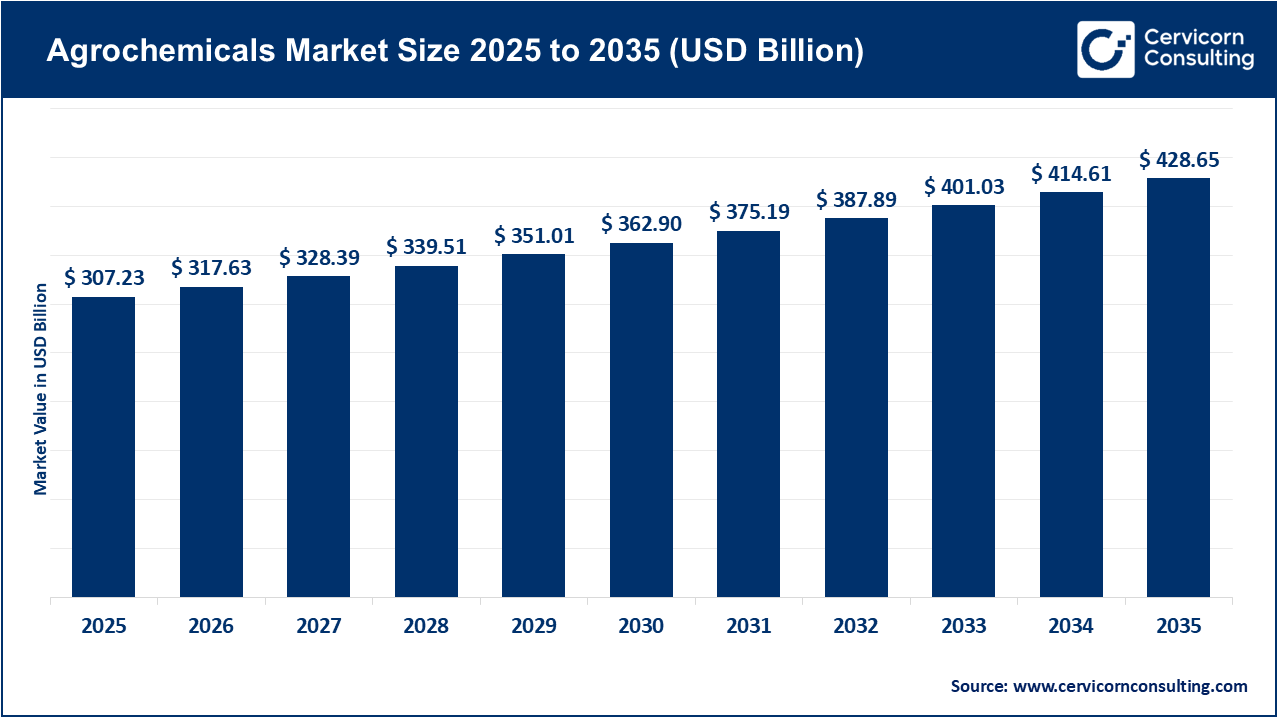

The global agrochemicals market size was worth USD 307.23 billion in 2025 and is anticipated to expand to around USD 428.65 billion by 2035, registering a compound annual growth rate (CAGR) of 3.4% from 2026 to 2035.

Agrochemicals Market Growth Factors

The agrochemicals market is expanding due to rising global food demand, shrinking arable land, and increasing pressure on farmers to maximize yield per hectare. Climate change intensifies pest and disease pressure, driving the need for reliable crop protection solutions. Technological advancements in formulation science, precision agriculture, seed treatments, and biologicals are also accelerating adoption. Government support programs, insurance schemes, and subsidies further boost demand, while trade dynamics influence supply and pricing. Simultaneously, stricter environmental regulations and increasing consumer awareness of food safety push companies toward safer chemistries and low-residue solutions. This combination of agronomic necessity, technological innovation, and regulatory evolution fuels ongoing market growth.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2828

What Is the Agrochemicals Market?

The agrochemicals market encompasses products used to enhance crop productivity and protect crops from pests, weeds, and diseases. These products include herbicides, insecticides, fungicides, nematicides, fumigants, plant growth regulators, seed treatments, and a wide range of adjuvants and additives that improve the effectiveness of active ingredients. It also includes emerging biological products such as microbial pesticides, plant extracts, RNA-based insect control tools, and biorational crop protection solutions. From R&D through manufacturing, distribution, and farmer advisory services, the agrochemicals market forms an integrated ecosystem that enables farmers to achieve consistent, high-quality yields.

Why Is the Agrochemicals Market Important?

Agrochemicals play a vital role in global food security. They help farmers reduce crop losses that would otherwise occur from pests, weeds, and pathogens. Without agrochemicals, global crop yields would drop significantly, leading to higher food prices, reduced export potential, and greater volatility in global food systems. These inputs allow mechanized, large-scale agriculture to function effectively and support global supply chains. Agrochemicals also protect public health by reducing vector-borne diseases (such as those spread by insects), stabilize farmer incomes, and support the agricultural economies of developing nations. The environmental impacts of these products make regulation essential, but with proper management and innovation, agrochemicals remain indispensable to sustainable food production.

Top Companies in the Agrochemicals Market

Below are detailed profiles of the major global companies that shape the agrochemicals market landscape. The sections include company specialization, focus areas, notable attributes, 2024 revenue, market position, and global presence.

1. Syngenta Group

Specialization:

Crop protection chemicals (herbicides, insecticides, fungicides), seed technologies, seed treatments, and advanced digital agriculture platforms.

Key Focus Areas:

• New chemistry development

• Biological solutions

• AI-driven precision agriculture

• Seed trait innovation

• Formulation and delivery systems

Notable Features:

• One of the world’s largest agrochemical and seed companies

• Strong in emerging markets due to tailored solutions for tropical agriculture

• Deep investment in sustainable and low-risk chemistries

2024 Revenue:

Approximately USD 28.8 billion.

Market Share Position:

Consistently ranked among the top two global crop protection companies.

Global Presence:

Operations in over 90 countries with strong market presence in Asia, Latin America, Europe, and North America.

2. Bayer AG (Crop Science Division)

Specialization:

Crop protection, seeds and traits, digital farming platforms, and biological solutions.

Key Focus Areas:

• Portfolio optimization

• New seed traits and herbicide-tolerant systems

• Sustainable pesticide innovations

• Digital crop monitoring

Notable Features:

• Extensive global R&D capabilities

• Large library of active ingredients

• Integrated crop solutions combining seeds and crop protection

2024 Revenue:

Crop Science division revenue was around EUR 22.3 billion.

Market Share Position:

A top-tier global leader in crop protection and seeds.

Global Presence:

Global network across Europe, the Americas, Asia Pacific, and Africa.

3. BASF SE (Agricultural Solutions)

Specialization:

Herbicides, fungicides, insecticides, seed treatments, and agricultural biologicals; specialty formulation additives and chemistries.

Key Focus Areas:

• Formulation innovation

• Lower-risk crop protection chemistries

• Digital agronomy partnerships

• Sustainable packaging and supply chain

Notable Features:

• Strong industrial chemistry foundation supporting agrochemical performance

• Focus on fungicides and seed treatments

2024 Revenue:

Agricultural Solutions segment reported around EUR 9.8 billion.

Market Share Position:

A top global player, among the top five in crop protection revenues.

Global Presence:

Significant footprint in Europe, North America, Latin America, and Asia.

4. Corteva, Inc.

Specialization:

Seeds, seed traits, crop protection (herbicides, insecticides, fungicides), biologicals, and digital agronomy technologies.

Key Focus Areas:

• Replacement chemistries to meet regulatory demand

• High-performance seed traits

• Biological crop protection portfolio expansion

• Integrated farmer solutions

Notable Features:

• Strongest integration of seeds + crop protection among major companies

• Post- DowDuPont restructuring directed toward innovation and farmer-centric tools

2024 Revenue:

Total revenue approximately USD 16.9 billion, with crop protection accounting for around USD 7.36 billion.

Market Share Position:

A global leader, especially strong in seeds and novel traits.

Global Presence:

Presence in over 100 countries, with major markets in North and South America, Europe, and Asia.

5. Dow Inc.

Specialization:

Adjuvants, surfactants, seed coatings, specialty formulation additives, and advanced chemical ingredients used by agrochemical manufacturers.

Key Focus Areas:

• High-performance formulation additives

• Seed coating polymers and binders

• Environmentally friendly surfactants

• Compatibility and stability technologies

Notable Features:

• Does not focus on active ingredients but is a major upstream supplier to agrochemical manufacturers

• Key supplier for formulation performance and efficiency

2024 Revenue:

Company-wide revenue approximately USD 43 billion (agro segment forms a subset).

Market Share Position:

Not a direct competitor in crop protection actives but a critical technology supplier in the value chain.

Global Presence:

Strong industrial footprint globally, supporting agricultural markets in all major farming regions.

Leading Trends and Their Market Impact

1. Transition to Safer and Low-Risk Chemistries

Regulators and consumers increasingly demand reduced environmental toxicity and residue levels. This is accelerating the replacement of older chemistries with modern, low-risk synthetic actives and biologicals. Companies redirect R&D toward microbials, RNA-based tools, botanical extracts, and biorational pesticides.

2. Growth of Biologicals

The global biologicals segment—biopesticides, bio-stimulants, and microbial inoculants—is growing at double-digit rates. Biologicals offer ecosystem-friendly alternatives and are especially important in high-value horticulture and organic farming.

3. Precision Agriculture Integration

Drones, satellite imaging, AI models, soil sensors, and variable-rate sprayers allow farmers to apply agrochemicals more precisely. This reduces waste and drift while improving performance. The trend favors products that integrate well with precision delivery systems.

4. Formulation Innovation

Adjuvants, surfactants, and controlled-release technologies increase active-ingredient efficacy, enabling reduced usage rates. Dow and BASF are key players in this domain.

5. Regulatory Tightening

Regions like the EU have introduced stringent pesticide-reduction targets. Regulatory approval timelines are lengthening, increasing development costs. Companies respond by prioritizing substitution chemistries and multi-mode-of-action actives.

6. Climate and Weather Uncertainty

Climate variability influences pest pressure and planting seasons. Extreme weather affects input purchase behavior, creating year-to-year demand volatility.

Successful Examples of Agrochemical Deployment Worldwide

Brazil – Rapid Product Approvals and Tropical Solutions

Brazil is one of the largest agrochemical markets thanks to its tropical climate, multiple crop seasons, and robust regulatory evolution. The country’s streamlined registration processes in recent years led to rapid commercialization of new products tailored to soybean, corn, and sugarcane.

North America – Precision Application Success

Farm cooperatives and private firms have deployed drone spraying, variable-rate application, and AI-supported scouting. These programs have reduced chemical use while maintaining or improving yields.

European Union – Integrated Pest Management (IPM)

Under sustainability frameworks, several EU nations have successfully implemented IPM to reduce dependency on chemical pesticides. Combining biological controls with selective chemistries has shown strong results for fruits, vegetables, and vineyards.

South America – Seed Treatment Leadership

Seed treatment adoption has surged in Brazil, Argentina, and the U.S., reducing losses during early growth stages while decreasing the need for foliar applications.

Global Regional Analysis and Policy Drivers

Europe (EU)

The EU’s Green Deal and Farm to Fork strategies aim to cut chemical pesticide use by up to 50% by 2030. This drives heavy investment in biologicals, precision agriculture, IPM techniques, and low-toxicity alternatives. Approval timelines are stricter, influencing company R&D priorities and product portfolios.

United States

The U.S. EPA’s evolving policies on pesticide registration, endangered species protection, and drift mitigation shape which products remain available. Regulatory reviews on specific active ingredients influence farmer adoption patterns. Digital agriculture adoption is strong due to robust infrastructure and high-tech farming incentives.

Brazil

Brazil’s updated pesticide legislation and record numbers of product registrations streamline market access. The country’s agricultural powerhouse status—leading in soybean, sugarcane, cotton, and corn—drives strong demand. However, environmental and public-health debates also intensify regulatory scrutiny.

India and South Asia

India’s updates to its Insecticides Rules and strict policies on MRLs directly influence product availability. The government encourages domestic manufacturing of agrochemicals, boosting capacity. Schemes such as crop insurance and subsidies support farmer purchasing power.

China and Southeast Asia

Asia Pacific remains the largest consumer market, driven by cropping intensity, multiple planting cycles, and high pest pressure. China’s domestic chemical production capacity influences global pricing and supply chain stability. Southeast Asian countries rely heavily on rice, palm oil, and fruits, sustaining consistent agrochemical demand.

Policy, Regulation, and Strategy Interaction

Government regulations are one of the most influential forces shaping company decisions. Key effects include:

Portfolio Realignment

Companies prioritize safer synthetic molecules, biologicals, and seed treatment technologies to comply with regional restrictions.

Increased Regulatory Investments

Manufacturers invest heavily in regulatory affairs, product stewardship, residue testing, and field trials to meet compliance standards across multiple regions.

Market Access Tactics

In markets like Brazil, companies fast-track new launches; in tightly regulated areas like the EU, they focus on substituted chemistries, integrated solutions, and IPM-compatible products.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Farm Equipment Market Growth Drivers, Trends, Key Players and Regional Insights by 2035