Material Handling Equipment Market Growth Drivers, Trends, Key Players and Regional Insights by 2035

Material Handling Equipment Market Size

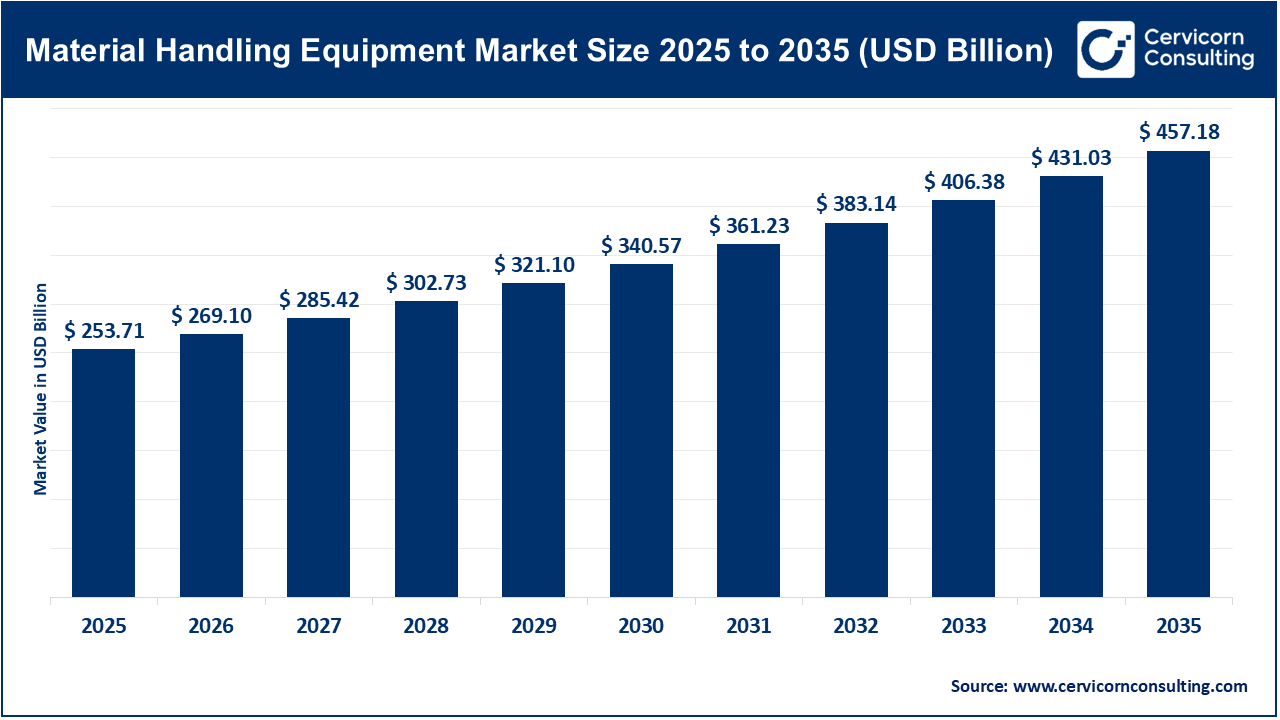

The global material handling equipment market size was worth USD 253.71 billion in 2025 and is anticipated to expand to around USD 457.18 billion by 2035, registering a compound annual growth rate (CAGR) of 6.1% from 2026 to 2035.

Material Handling Equipment Market — Growth Factors

The material handling equipment market is expanding due to a combination of technological, economic, and structural forces. Key drivers include booming e-commerce and omni-channel retail that demand rapid, accurate, and high-volume order fulfillment; rising labour shortages and higher labour costs pushing industries toward warehouse automation; Industry 4.0 initiatives integrating robotics, IoT, AI, and advanced WMS/WCS software for optimized intralogistics; reshoring and nearshoring manufacturing that increases the need for flexible, modern warehousing; sustainability trends driving the adoption of energy-efficient electric forklifts and low-emission equipment; and government-led infrastructure programs supporting digitalization and supply-chain modernization. These drivers collectively accelerate capital investments in automated systems, robotics, material movement technologies, and lifecycle service models.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2825

What Is the Material Handling Equipment Market?

The material handling equipment market consists of all systems, machinery, and software used to move, store, control, and protect goods throughout the manufacturing, warehousing, and distribution cycle. It includes mobile equipment (such as forklifts, pallet trucks, tow tractors), fixed equipment (conveyors, cranes, racking systems, sorters, AS/RS units), and digital technologies (warehouse management systems, warehouse control systems, analytics and orchestration platforms). The market covers equipment manufacturing, installation, after-sales services, maintenance, retrofits, spare parts, and increasingly, subscription-based robotics or automation-as-a-service (RaaS). Customers span industries like automotive, retail, e-commerce, food processing, airports, parcel hubs, pharmaceuticals, and electronics. The ecosystem blends heavy-duty industrial machinery with high-tech robotics and software, making it one of the most dynamic segments within industrial automation.

Why Material Handling Equipment Is Important

Material handling equipment is essential for supply-chain efficiency, cost optimization, safety, and resilience. It minimizes manual labour, reduces handling time, and boosts accuracy in order picking and fulfillment. Automated systems help companies meet rising customer expectations for same-day or next-day deliveries, while improving inventory control, space utilization, and energy efficiency. MHE also supports workplace safety by reducing manual lifting and movement of heavy materials. For industries with high throughput or high regulatory requirements — such as grocery, pharmaceuticals, or automotive manufacturing — material handling solutions are critical to maintaining quality, speed, and consistency. In a world increasingly reliant on e-commerce and complex global logistics, modern material handling equipment is no longer optional; it is a strategic enabler of competitive advantage.

Material Handling Equipment Market — Top Companies

Below are the top global companies shaping the material handling equipment landscape, along with their specializations, focus areas, features, revenue (latest available), market share context, and global presence.

1. Daifuku Co., Ltd.

Company: Daifuku Co., Ltd. (Japan)

Specialization: Automated material handling systems, AS/RS, conveyors, sorters, baggage handling, and factory automation.

Key Focus Areas: Warehouse automation, airport baggage systems, manufacturing automation, and lifecycle services.

Notable Features: Global systems integrator with strong execution capabilities, extensive airport automation footprint, strong service and maintenance business.

2024 Revenue: ¥563,228 million (FY2024 consolidated).

Market Share & Global Presence: Among the largest global MHE system integrators with significant presence in Asia, Europe, and North America.

2. Murata Machinery Ltd. (Muratec)

Company: Murata Machinery, Ltd. (Japan)

Specialization: Logistics automation, AS/RS, factory automation, semiconductor fab automation, machine tools, textile machinery.

Key Focus Areas: Semiconductor and electronics automation, intralogistics systems, AGVs, advanced factory automation.

Notable Features: Deep engineering expertise, strong position in semiconductor and high-precision manufacturing automation.

2024 Revenue: Approximately ¥526,076 million (for the year ending March 31, 2025).

Market Share & Global Presence: Strong reach across Asia, with fast-growing presence in global semiconductor supply chains.

3. Vanderlande Industries B.V.

Company: Vanderlande (Netherlands) — Part of Toyota Industries

Specialization: Warehouse automation, high-throughput sortation, airport baggage handling, parcel and postal automation.

Key Focus Areas: E-commerce fulfillment systems, baggage handling at global airports, pallet/parcel handling, automation software.

Notable Features: Leading integrator with large airport and parcel hub projects, supported by Toyota’s scale and investment strength.

2024 Revenue: Approximately €2.3 billion.

Market Share & Global Presence: Strong in Europe, North America, Middle East, and Asia with installations in major airports and parcel networks worldwide.

4. Honeywell International Inc.

Company: Honeywell International Inc. (USA)

Specialization: Warehouse automation technologies, sensors, industrial software, controls, and material handling systems through Honeywell Intelligrated.

Key Focus Areas: Warehouse execution software, robotics partnerships, automation controls, advanced sensing solutions.

Notable Features: Large industrial footprint, diversified technology portfolio, strong integration of hardware and industrial digital solutions.

2024 Revenue: $38.49 billion (total Honeywell sales).

Market Share & Global Presence: Extensive global presence across Americas, Europe, and APAC, with significant warehouse automation deployments.

5. KION Group AG

Company: KION Group AG (Germany)

Specialization: Forklifts, warehouse trucks, AGVs, automation systems, software (brands include Linde and STILL).

Key Focus Areas: Industrial trucks, fleet services, automation, robotics, and digital intralogistics solutions.

Notable Features: One of the world’s largest forklift manufacturers; vertically integrated portfolio combining trucks, software, and automation.

2024 Revenue: €11.5 billion.

Market Share & Global Presence: Strong presence across Europe, Americas, and Asia; leading provider of forklifts and warehouse equipment globally.

Leading Trends and Their Impact

1. Rise of Warehousing Robotics & Goods-to-Person Systems

Autonomous mobile robots (AMRs), automated guided vehicles (AGVs), robotic picking arms, and goods-to-person AS/RS solutions significantly reduce travel time and labour dependency. Warehouses adopting robotics experience dramatic increases in throughput, especially in e-commerce and grocery fulfillment.

2. Integration of AI, Analytics & Orchestration Platforms

AI-driven demand forecasting, dynamic slotting, and fleet orchestration software optimize storage, picking, and traffic control. Predictive maintenance enhances uptime and extends equipment lifespan.

3. Electrification & Sustainable MHE

Electric forklifts, lithium-ion battery systems, rapid charging, and hydrogen fuel cell forklifts reduce emissions and improve cost efficiency. Sustainability standards push companies to upgrade older fleets.

4. Autonomous Intralogistics & 5G/Edge Technologies

5G-enabled fleets allow large operations to run highly coordinated AMR/AGV networks with improved safety and real-time navigation, reducing dependency on fixed infrastructure.

5. Micro-Fulfillment & Last-Mile Optimization

Companies are adopting smaller, automated urban micro-fulfillment centers to improve delivery speeds. This drives demand for compact AS/RS, vertical lift modules, and high-density storage systems.

6. Lifecycle Services & RaaS

Robotics-as-a-service and long-term service contracts shift revenue from one-time capital purchases to recurring models. This trend helps companies adopt automation with lower upfront costs.

Successful Global Examples of Material Handling Implementations

Amazon (USA)

Amazon’s large-scale robotics adoption began with Kiva robots and has evolved into advanced mobile robotic fleets with AI-driven orchestration. This drastically reduced walking time and enabled ultra-fast fulfillment cycles.

Ocado (UK)

Ocado’s grid-based robots and highly automated Customer Fulfilment Centres (CFCs) set global benchmarks in grocery automation. The system is now licensed globally through the Ocado Smart Platform.

Inditex (Zara, Spain)

Zara uses heavily automated warehouses and goods-to-person systems to support fast-fashion inventory turnover, enabling rapid store replenishment across hundreds of markets.

Vanderlande at Global Airports

Vanderlande’s baggage handling systems support major airports worldwide, enabling fast, reliable, and safe passenger baggage movement at extremely high volumes.

BMW Group Factories

BMW plants use AGVs, automated tuggers, and intelligent logistics traffic control to optimize in-plant material flow for both electric and internal combustion engine production lines.

Global Regional Analysis — Government Initiatives and Policies Shaping the Market

North America (US & Canada)

Key Drivers:

- Large e-commerce customer base

- Reshoring of manufacturing

- Strong investment in logistics and transportation modernization

Government Influence:

- Infrastructure investment laws supporting transportation hubs and digitalization

- Incentives for manufacturing automation and electrification

- Grants for modern warehousing, clean energy equipment, and logistics innovation

Impact:

These policies accelerate the adoption of warehouse automation, electric forklifts, fleet management technology, and robotics.

Europe (EU & UK)

Key Drivers:

- Sustainability and emissions regulations

- High labour costs

- Focus on operational efficiency in supply chains

Government Influence:

- EU funding programs for robotics, AI, and digital transformation

- Energy efficiency standards driving fleet electrification

- Research grants supporting next-generation intralogistics technologies

Impact:

European governments play a crucial role in accelerating warehouse automation and green equipment adoption.

China & East Asia

Key Drivers:

- Rapid e-commerce expansion

- Automation-focused national strategies

- Manufacturing modernization

Government Influence:

- Industrial policies supporting robotics and smart manufacturing

- Subsidies encouraging domestic MHE production

- Large-scale logistics hub development

Impact:

Fastest-growing region for warehouse automation, dominated by both global and domestic solution providers.

India & South Asia

Key Drivers:

- Expanding e-commerce and retail networks

- Modern logistics parks and industrial corridors

- Growing 3PL and manufacturing ecosystems

Government Influence:

- National Logistics Policy

- PLI schemes for manufacturing competitiveness

- Investments in digital logistics platforms and multimodal transport

Impact:

Increasing adoption of automation, especially in large distribution centers and industrial clusters.

Middle East, Africa & Latin America

Key Drivers:

- Growing retail and e-commerce

- Infrastructure modernization

- Investment in trade hubs and free zones

Government Influence:

- National visions (e.g., GCC countries) promoting smart logistics

- Infrastructure investments in ports, warehouses, and airports

Impact:

Steady growth in automated solutions, focused on scalable and modular MHE technologies.

Market Scale & Outlook

- The global material handling equipment market was valued in the hundreds of billions of dollars in 2024.

- Forecasts indicate steady mid-single-digit to low double-digit CAGR over the next decade.

- Market growth is driven by warehouse automation, digital transformation, robotics adoption, sustainability requirements, and expanding e-commerce.

- Suppliers increasingly focus on software, lifecycle services, and automation-as-a-service to meet evolving customer needs.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Video Streaming Market Growth Drivers, Trends, Key Players and Regional Insights by 2035