Metal Recycling Market Revenue, Trends, and Strategic Insights by 2035

Metal Recycling Market Size

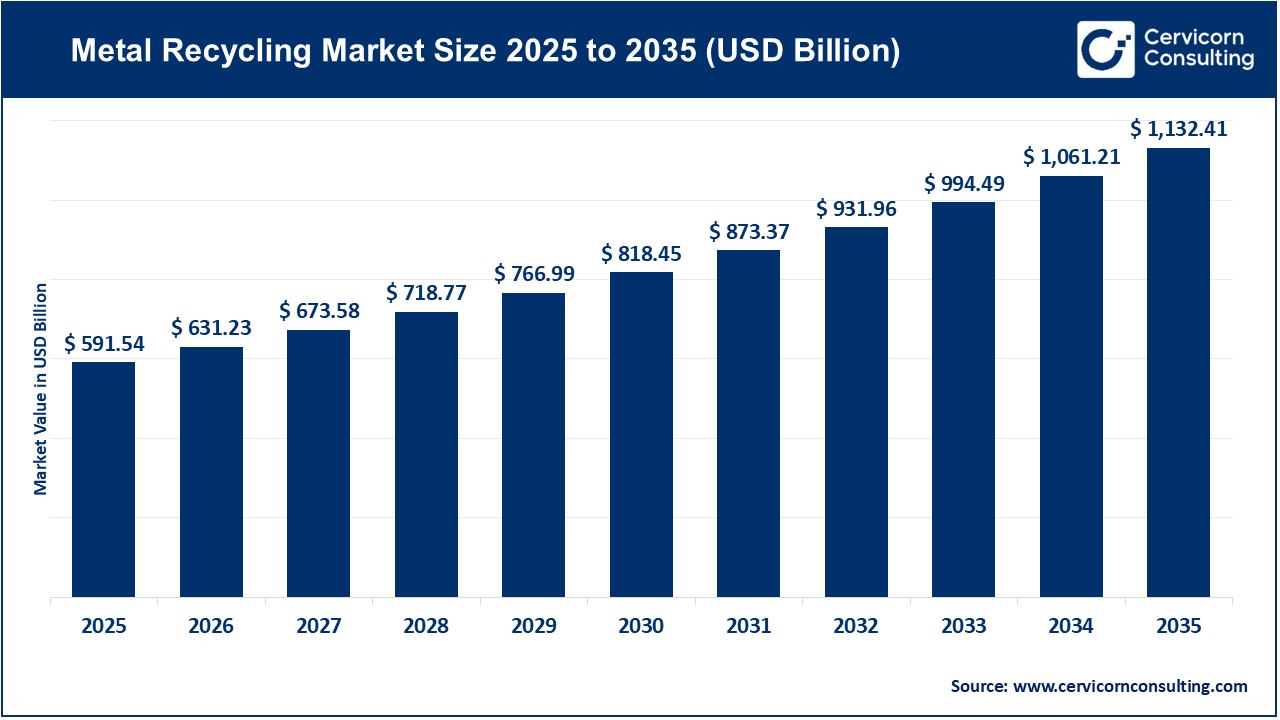

The global metal recycling market reached an estimated valuation of USD 594.54 billion in 2025 and is projected to grow substantially, attaining approximately USD 1,132.41 billion by 2035. This growth reflects a strong compound annual growth rate (CAGR) of around 6.71% throughout the forecast period.

What Is the Metal Recycling Market?

The metal recycling market refers to the global industry involved in collecting, processing, refining, and reintroducing scrap metal into the manufacturing supply chain. It includes both ferrous metals (such as steel and iron) and non-ferrous metals (such as aluminum, copper, lead, zinc, nickel, and precious metals). The process typically involves collection from end-of-life vehicles, industrial scrap, construction debris, consumer products, and electronic waste, followed by sorting, shredding, melting, and purification before reuse in manufacturing.

Unlike many materials, metals can be recycled indefinitely without losing their structural integrity. This makes metal recycling one of the most efficient and sustainable components of the global circular economy. The industry supports sectors such as automotive, construction, packaging, aerospace, electronics, shipbuilding, and heavy machinery manufacturing.

Globally, the metal recycling market represents a multi-hundred-billion-dollar industry and continues to expand as sustainability regulations tighten and industries transition toward low-carbon production models.

Metal Recycling Market Growth Factors

The metal recycling market is experiencing strong growth driven by increasing global demand for sustainable raw materials, rising environmental regulations aimed at reducing carbon emissions, growing industrialization in emerging economies, expanding infrastructure and construction activities, and the cost advantages associated with recycled metals over virgin ore extraction; technological advancements such as AI-based sorting systems, automated separation technologies, and sensor-driven material identification are improving recovery efficiency and profitability.

The surge in electric vehicle production and renewable energy infrastructure is boosting demand for copper and aluminum recycling; urban mining and e-waste recycling are unlocking high-value metal streams; government initiatives promoting circular economy frameworks are accelerating recycling adoption; and supply chain disruptions in mined raw materials are encouraging manufacturers to secure secondary metal sources, collectively propelling sustained market expansion worldwide.

Why the Metal Recycling Market Is Important

1. Environmental Sustainability

Recycling metals significantly reduces energy consumption compared to mining and refining virgin ores. For example, recycling aluminum can save up to 95% of the energy required to produce new aluminum. Steel recycling also cuts energy use and greenhouse gas emissions substantially. These savings contribute directly to climate change mitigation and carbon neutrality goals.

2. Resource Conservation

Metal ores are finite resources. Recycling extends the lifecycle of existing materials and reduces dependence on environmentally disruptive mining operations. This helps preserve ecosystems and reduces water and soil pollution.

3. Economic Benefits

Recycled metals are often cheaper than primary metals. This cost efficiency benefits manufacturers while stabilizing supply chains. The industry also creates employment opportunities in collection, processing, logistics, and advanced manufacturing.

4. Circular Economy Enablement

Metal recycling is a cornerstone of the circular economy model, where materials are reused continuously rather than discarded. Governments and corporations increasingly integrate recycling into sustainability strategies to reduce landfill waste and improve material efficiency.

Major Companies in the Metal Recycling Market

1. Sims Limited

Specialization

Sims Limited is one of the world’s largest metal and electronics recycling companies. It operates through divisions focused on ferrous and non-ferrous scrap recycling, electronics recovery, and resource renewal solutions.

Key Focus Areas

- Ferrous and non-ferrous scrap processing

- Electronics recycling and IT asset disposition

- Advanced material recovery technologies

- Circular economy partnerships

Notable Features

- Over a century of operational experience

- Strong ESG and sustainability focus

- Integrated recycling and trading networks

2024 Revenue

Approximately USD 7.5 billion in annual revenue (FY2024).

Market Share

Among the top global scrap metal recyclers, particularly strong in ferrous scrap markets.

Global Presence

Operations across North America, Europe, Australia, and New Zealand, with extensive export capabilities.

2. ArcelorMittal

Specialization

ArcelorMittal is the world’s largest steel producer and a major recycler of ferrous scrap integrated into its steelmaking operations.

Key Focus Areas

- Electric Arc Furnace (EAF) steel production

- Scrap metal sourcing and processing

- Carbon reduction strategies

Notable Features

- Heavy investment in green steel initiatives

- High recycled scrap usage in European operations

- Strong vertical integration

2024 Revenue

Group revenue exceeds USD 60 billion globally (steel and related operations).

Market Share

Dominant global steel producer with significant indirect influence over global scrap demand.

Global Presence

Operations in over 60 countries across Europe, North America, South America, Asia, and Africa.

3. Nucor Corporation

Specialization

Nucor is the largest recycler of steel in the Western Hemisphere and a leading steel manufacturer utilizing electric arc furnace technology.

Key Focus Areas

- Scrap steel recycling

- EAF steel production

- Domestic scrap supply chain integration

Notable Features

- Processes more than 25 million metric tons of recycled steel annually

- Owns major scrap processor subsidiaries

- Leader in low-carbon steel production

2024 Revenue

Annual revenues exceeding USD 30 billion.

Market Share

One of the largest scrap steel consumers globally.

Global Presence

Primarily United States-focused with international trading networks.

4. Aurubis AG

Specialization

Aurubis is Europe’s largest copper producer and a global leader in non-ferrous metal recycling.

Key Focus Areas

- Copper recycling and refining

- Complex scrap processing

- Precious metal recovery

Notable Features

- Advanced smelting technology

- Large-scale recycling facilities in Europe and North America

- Significant investment in U.S. recycling expansion

2024 Revenue

Approximately €18 billion in annual revenue.

Market Share

Strong position in global copper recycling and refining markets.

Global Presence

Operations across Europe and North America, with global trading partnerships.

5. European Metal Recycling (EMR)

Specialization

European Metal Recycling (EMR) is one of the largest scrap metal recyclers in Europe.

Key Focus Areas

- Ferrous and non-ferrous scrap processing

- Industrial metal recovery

- High-volume shredding and sorting

Notable Features

- Advanced sorting and shredding facilities

- Strong partnerships with steel mills and foundries

- Sustainability-driven operations

2024 Revenue

Privately held; estimated multi-billion-dollar annual turnover.

Market Share

Major contributor to Europe’s scrap metal supply.

Global Presence

Primarily Europe and the UK, with international trading operations.

Leading Trends and Their Impact

1. Advanced Sorting and Automation

AI-powered sorting systems, robotics, and sensor-based separation technologies are improving metal purity and recovery rates. This enhances profitability and reduces contamination.

2. Growth of Electric Arc Furnace Steelmaking

EAF technology relies heavily on scrap metal and emits significantly less carbon than blast furnaces. The shift toward EAF steelmaking is accelerating scrap demand globally.

3. Urban Mining and E-Waste Recycling

The recovery of valuable metals from electronic waste and end-of-life vehicles is expanding. Copper, aluminum, lithium, and rare metals are increasingly extracted from secondary sources.

4. ESG and Carbon Neutrality Commitments

Corporations are integrating recycled metals into procurement strategies to meet carbon reduction targets. Recycled inputs are becoming mandatory in certain regulatory frameworks.

5. Supply Chain Resilience

Geopolitical tensions and raw material volatility are encouraging nations to strengthen domestic recycling systems to reduce dependency on imported ores.

Successful Examples of Metal Recycling Around the World

Europe’s Integrated Scrap Ecosystem

European nations have built highly organized recycling infrastructures supported by strict waste directives and circular economy mandates. Steel producers widely utilize scrap in EAFs, reducing emissions and import dependence.

United States EAF Steel Leadership

The U.S. leads in electric arc furnace steel production, with companies like Nucor demonstrating how scrap recycling can anchor a modern steel industry.

Japan’s Advanced Scrap Sorting

Japan utilizes high-precision separation technology to maximize material recovery, particularly in automotive and electronics recycling.

China’s Scrap Reform Policies

China has transitioned toward greater domestic scrap utilization to reduce pollution from primary steelmaking and improve environmental performance.

Global Regional Analysis Including Government Initiatives

Asia-Pacific

Asia-Pacific dominates the metal recycling market due to industrial growth and large steel production capacity. Countries such as China and India are strengthening scrap import policies and boosting domestic recycling capacity. Government initiatives focus on expanding electric arc furnace steel production and formalizing scrap collection systems.

Key Government Initiatives

- Promotion of EAF steelmaking

- Stricter environmental controls on mining

- Policies encouraging domestic scrap processing

Europe

Europe leads in regulatory frameworks promoting recycling. The European Green Deal and circular economy action plans emphasize recycled content targets and reduced scrap exports.

Key Government Initiatives

- Waste Framework Directive

- Carbon reduction targets for heavy industry

- Incentives for recycled material usage

North America

The United States and Canada benefit from established recycling infrastructure and high EAF penetration rates. Policies support domestic metal production and infrastructure development.

Key Government Initiatives

- Infrastructure investment programs

- Incentives for sustainable manufacturing

- Tariffs encouraging domestic steel recycling

Latin America

Developing recycling infrastructure with increasing formalization of scrap markets. Government policies aim to modernize waste management systems and encourage foreign investment in recycling plants.

What Is the Metal Recycling Market?

The metal recycling market refers to the global industry involved in collecting, processing, refining, and reintroducing scrap metal into the manufacturing supply chain. It includes both ferrous metals (such as steel and iron) and non-ferrous metals (such as aluminum, copper, lead, zinc, nickel, and precious metals). The process typically involves collection from end-of-life vehicles, industrial scrap, construction debris, consumer products, and electronic waste, followed by sorting, shredding, melting, and purification before reuse in manufacturing.

Unlike many materials, metals can be recycled indefinitely without losing their structural integrity. This makes metal recycling one of the most efficient and sustainable components of the global circular economy. The industry supports sectors such as automotive, construction, packaging, aerospace, electronics, shipbuilding, and heavy machinery manufacturing.

Globally, the metal recycling market represents a multi-hundred-billion-dollar industry and continues to expand as sustainability regulations tighten and industries transition toward low-carbon production models.

Metal Recycling Market Growth Factors

The metal recycling market is experiencing strong growth driven by increasing global demand for sustainable raw materials, rising environmental regulations aimed at reducing carbon emissions, growing industrialization in emerging economies, expanding infrastructure and construction activities, and the cost advantages associated with recycled metals over virgin ore extraction; technological advancements such as AI-based sorting systems, automated separation technologies, and sensor-driven material identification are improving recovery efficiency and profitability.

The surge in electric vehicle production and renewable energy infrastructure is boosting demand for copper and aluminum recycling; urban mining and e-waste recycling are unlocking high-value metal streams; government initiatives promoting circular economy frameworks are accelerating recycling adoption; and supply chain disruptions in mined raw materials are encouraging manufacturers to secure secondary metal sources, collectively propelling sustained market expansion worldwide.

Why the Metal Recycling Market Is Important

1. Environmental Sustainability

Recycling metals significantly reduces energy consumption compared to mining and refining virgin ores. For example, recycling aluminum can save up to 95% of the energy required to produce new aluminum. Steel recycling also cuts energy use and greenhouse gas emissions substantially. These savings contribute directly to climate change mitigation and carbon neutrality goals.

2. Resource Conservation

Metal ores are finite resources. Recycling extends the lifecycle of existing materials and reduces dependence on environmentally disruptive mining operations. This helps preserve ecosystems and reduces water and soil pollution.

3. Economic Benefits

Recycled metals are often cheaper than primary metals. This cost efficiency benefits manufacturers while stabilizing supply chains. The industry also creates employment opportunities in collection, processing, logistics, and advanced manufacturing.

4. Circular Economy Enablement

Metal recycling is a cornerstone of the circular economy model, where materials are reused continuously rather than discarded. Governments and corporations increasingly integrate recycling into sustainability strategies to reduce landfill waste and improve material efficiency.

Major Companies in the Metal Recycling Market

1. Sims Limited

Specialization

Sims Limited is one of the world’s largest metal and electronics recycling companies. It operates through divisions focused on ferrous and non-ferrous scrap recycling, electronics recovery, and resource renewal solutions.

Key Focus Areas

- Ferrous and non-ferrous scrap processing

- Electronics recycling and IT asset disposition

- Advanced material recovery technologies

- Circular economy partnerships

Notable Features

- Over a century of operational experience

- Strong ESG and sustainability focus

- Integrated recycling and trading networks

2024 Revenue

Approximately USD 7.5 billion in annual revenue (FY2024).

Market Share

Among the top global scrap metal recyclers, particularly strong in ferrous scrap markets.

Global Presence

Operations across North America, Europe, Australia, and New Zealand, with extensive export capabilities.

2. ArcelorMittal

Specialization

ArcelorMittal is the world’s largest steel producer and a major recycler of ferrous scrap integrated into its steelmaking operations.

Key Focus Areas

- Electric Arc Furnace (EAF) steel production

- Scrap metal sourcing and processing

- Carbon reduction strategies

Notable Features

- Heavy investment in green steel initiatives

- High recycled scrap usage in European operations

- Strong vertical integration

2024 Revenue

Group revenue exceeds USD 60 billion globally (steel and related operations).

Market Share

Dominant global steel producer with significant indirect influence over global scrap demand.

Global Presence

Operations in over 60 countries across Europe, North America, South America, Asia, and Africa.

3. Nucor Corporation

Specialization

Nucor is the largest recycler of steel in the Western Hemisphere and a leading steel manufacturer utilizing electric arc furnace technology.

Key Focus Areas

- Scrap steel recycling

- EAF steel production

- Domestic scrap supply chain integration

Notable Features

- Processes more than 25 million metric tons of recycled steel annually

- Owns major scrap processor subsidiaries

- Leader in low-carbon steel production

2024 Revenue

Annual revenues exceeding USD 30 billion.

Market Share

One of the largest scrap steel consumers globally.

Global Presence

Primarily United States-focused with international trading networks.

4. Aurubis AG

Specialization

Aurubis is Europe’s largest copper producer and a global leader in non-ferrous metal recycling.

Key Focus Areas

- Copper recycling and refining

- Complex scrap processing

- Precious metal recovery

Notable Features

- Advanced smelting technology

- Large-scale recycling facilities in Europe and North America

- Significant investment in U.S. recycling expansion

2024 Revenue

Approximately €18 billion in annual revenue.

Market Share

Strong position in global copper recycling and refining markets.

Global Presence

Operations across Europe and North America, with global trading partnerships.

5. European Metal Recycling (EMR)

Specialization

European Metal Recycling (EMR) is one of the largest scrap metal recyclers in Europe.

Key Focus Areas

- Ferrous and non-ferrous scrap processing

- Industrial metal recovery

- High-volume shredding and sorting

Notable Features

- Advanced sorting and shredding facilities

- Strong partnerships with steel mills and foundries

- Sustainability-driven operations

2024 Revenue

Privately held; estimated multi-billion-dollar annual turnover.

Market Share

Major contributor to Europe’s scrap metal supply.

Global Presence

Primarily Europe and the UK, with international trading operations.

Leading Trends and Their Impact

1. Advanced Sorting and Automation

AI-powered sorting systems, robotics, and sensor-based separation technologies are improving metal purity and recovery rates. This enhances profitability and reduces contamination.

2. Growth of Electric Arc Furnace Steelmaking

EAF technology relies heavily on scrap metal and emits significantly less carbon than blast furnaces. The shift toward EAF steelmaking is accelerating scrap demand globally.

3. Urban Mining and E-Waste Recycling

The recovery of valuable metals from electronic waste and end-of-life vehicles is expanding. Copper, aluminum, lithium, and rare metals are increasingly extracted from secondary sources.

4. ESG and Carbon Neutrality Commitments

Corporations are integrating recycled metals into procurement strategies to meet carbon reduction targets. Recycled inputs are becoming mandatory in certain regulatory frameworks.

5. Supply Chain Resilience

Geopolitical tensions and raw material volatility are encouraging nations to strengthen domestic recycling systems to reduce dependency on imported ores.

Successful Examples of Metal Recycling Around the World

Europe’s Integrated Scrap Ecosystem

European nations have built highly organized recycling infrastructures supported by strict waste directives and circular economy mandates. Steel producers widely utilize scrap in EAFs, reducing emissions and import dependence.

United States EAF Steel Leadership

The U.S. leads in electric arc furnace steel production, with companies like Nucor demonstrating how scrap recycling can anchor a modern steel industry.

Japan’s Advanced Scrap Sorting

Japan utilizes high-precision separation technology to maximize material recovery, particularly in automotive and electronics recycling.

China’s Scrap Reform Policies

China has transitioned toward greater domestic scrap utilization to reduce pollution from primary steelmaking and improve environmental performance.

Global Regional Analysis Including Government Initiatives

Asia-Pacific

Asia-Pacific dominates the metal recycling market due to industrial growth and large steel production capacity. Countries such as China and India are strengthening scrap import policies and boosting domestic recycling capacity. Government initiatives focus on expanding electric arc furnace steel production and formalizing scrap collection systems.

Key Government Initiatives

- Promotion of EAF steelmaking

- Stricter environmental controls on mining

- Policies encouraging domestic scrap processing

Europe

Europe leads in regulatory frameworks promoting recycling. The European Green Deal and circular economy action plans emphasize recycled content targets and reduced scrap exports.

Key Government Initiatives

- Waste Framework Directive

- Carbon reduction targets for heavy industry

- Incentives for recycled material usage

North America

The United States and Canada benefit from established recycling infrastructure and high EAF penetration rates. Policies support domestic metal production and infrastructure development.

Key Government Initiatives

- Infrastructure investment programs

- Incentives for sustainable manufacturing

- Tariffs encouraging domestic steel recycling

Latin America

Developing recycling infrastructure with increasing formalization of scrap markets. Government policies aim to modernize waste management systems and encourage foreign investment in recycling plants.

Middle East & Africa

Emerging recycling markets driven by construction growth and industrial diversification. Governments are investing in industrial zones and sustainability strategies to promote recycling industries.

Emerging recycling markets driven by construction growth and industrial diversification. Governments are investing in industrial zones and sustainability strategies to promote recycling industries.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Steel Plate Market Revenue, Trends, and Strategic Insights by 2035