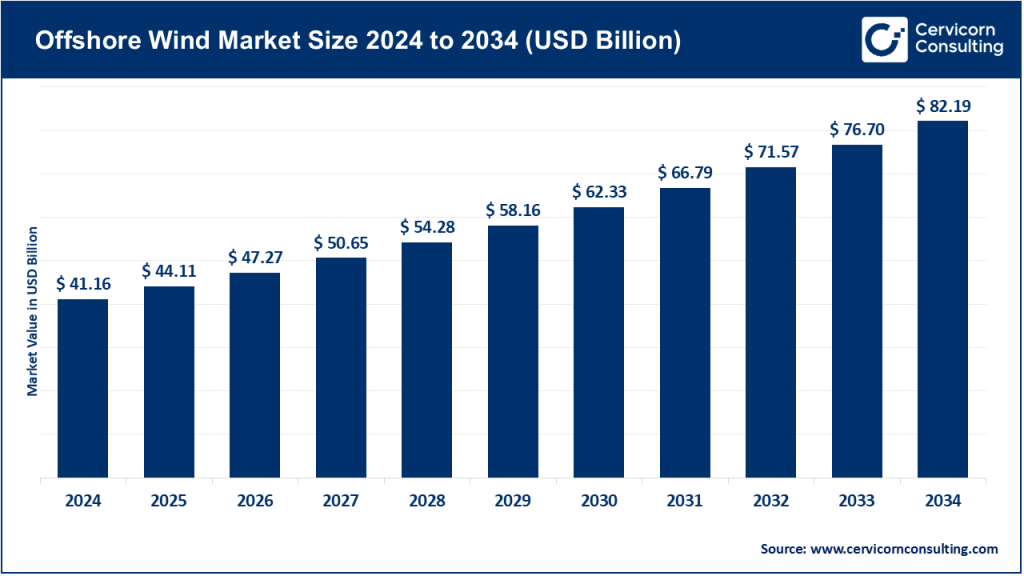

Offshore Wind Market Size

What is the offshore wind market?

The offshore wind market covers the development, construction, installation, operation and servicing of wind farms located in marine environments (coastal and deeper waters). It includes the manufacturing and sale of offshore wind turbines and foundations, subsea and onshore grid connection (export cables, substations), installation vessels and logistics, O&M (operations & maintenance) services, financing, and the enabling supply chain: port upgrades, heavy-lift vessels, specialized foundations (monopiles, jackets, floating platforms), and grid reinforcement. Unlike onshore wind, offshore projects tap stronger and steadier winds, enabling larger turbines and higher capacity factors — but they also require greater capital, specialized logistics and different permitting and environmental assessments.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2745

Why is offshore wind important?

Offshore wind plays a strategic role in decarbonizing power systems because it can deliver very large amounts of clean, firm-capable electricity close to major coastal demand centers. Its importance springs from three practical advantages: (1) higher and steadier wind speeds offshore raise the energy yield per turbine; (2) the ability to deploy very large turbines and vast arrays makes it efficient at grid-scale capacity additions.

(3) coastal siting reduces the distance between bulk generation and major load centers (cities and industrial clusters). For countries with constrained onshore options or ambitious power-sector decarbonization targets, offshore wind is often the fastest route to gigawatt-scale renewables additions. Public policy interest and private capital flows (from developers, infrastructure funds and utilities) reflect this central role in energy transition planning.

Offshore wind market — Growth factors

Rapid cost declines from larger, more efficient turbines and better project design; stronger long-term policy commitments (auctions, CfDs, feed-in and permitting reforms); expansion of floating offshore wind enabling deeper-water sites; electrification demand from coastal industry and data centers; improvements in subsea cable and grid technologies easing transmission integration; growing private capital and institutional investment hungry for long-term predictable cash flows; dedicated port and vessel investments that shrink logistics bottlenecks; industrial policy and local-content requirements that stimulate regional manufacturing, and climate-driven urgency and energy-security considerations (diversifying away from volatile fossil-fuel imports) — together these technical, economic and political drivers are creating a virtuous circle of larger projects, faster build schedules and growing supply-chain scale that accelerate deployment worldwide.

Offshore Wind Market — Top Companies

Below are concise profiles of the five companies you specified: specialization, key focus areas, notable features, 2024 revenue context (company-level reporting, not exclusively offshore), market presence and a note on market share posture where available.

Note on revenues & market share: Many large corporations report consolidated revenues across multiple energy businesses; the figures below reference 2024 company or segment reporting where possible. Offshore wind revenues are usually embedded within broader renewables or energy segments — exact offshore-only revenue splits are not always disclosed publicly.

1) General Electric (GE Vernova / GE Renewable Energy)

- Specialization: Full-scope wind turbine manufacturing (notably large direct-drive and multi-MW machines), offshore wind turbines (Haliade / GE Offshore technology), electrical equipment and services.

- Key focus areas: Large 12-20+ MW-class offshore turbines, project supply for U.S. and European projects, turbine services and digital O&M.

- Notable features: GE Vernova is the umbrella for GE’s power and renewables businesses; GE supplied the Haliade X platform used in major projects such as Vineyard Wind 1.

- 2024 revenue (company/segment context): GE Vernova reported multi-billion dollar revenue (around $35 billion across power and renewable assets in 2024).

- Market share & global presence: Strong presence in North America and selected European projects; competes with Siemens Gamesa and Vestas for major project wins. Market share in offshore turbinemaking is significant for specific product niches (very large turbines), though exact global share fluctuates with tender wins.

2) Vestas

- Specialization: Wind turbines (primarily onshore historically), growing offshore involvement through product lines, end-to-end services (installation, service contracts).

- Key focus areas: Reliable global supply chain for turbine components, service and repowering markets, scaling manufacturing and logistics to support large projects.

- Notable features: Longstanding industry leader in onshore wind with expanding offshore ambitions and integrated service offerings.

- 2024 revenue (company context): Vestas reported robust revenue for 2024 in its annual statements, maintaining its position as one of the world’s largest wind turbine manufacturers.

- Market share & global presence: Globally distributed operations and service footprint; strong in Europe and expanding in Asia and the Americas via service and partnership strategies.

3) Shanghai Electric Wind Power Equipment Co. (Shanghai Electric)

- Specialization: Large-scale turbines and power equipment manufacturing, strong presence in China’s wind market, including offshore-capable models.

- Key focus areas: Domestic Chinese projects, exports where feasible, integration with broader energy systems (nuclear, thermal, grid equipment).

- Notable features: Part of a broad industrial conglomerate with scale in heavy machinery and power-plant equipment; leverages China’s fast-expanding offshore pipeline.

- 2024 revenue (company context): Shanghai Electric reported notable 2024 revenue growth, driven by clean-energy businesses.

- Market share & global presence: Leadership in China’s domestic market (a top manufacturer there) and growing export ambitions; China is becoming one of the largest offshore markets globally.

4) Siemens Gamesa (Siemens Energy / Siemens Gamesa Renewable Energy)

- Specialization: Offshore turbine design and manufacture (offshore nacelles, blades, and foundations integration), strong presence in major European projects.

- Key focus areas: Large-scale offshore turbine platforms (e.g., SG-series), supply to major European projects, manufacturing footprint in Europe (including UK facilities).

- Notable features: Siemens Gamesa is a go-to supplier for many of the largest North Sea projects; parent company Siemens Energy reports strong revenue contributions from Grid Technologies and Siemens Gamesa ramp-ups.

- 2024 revenue (company/segment context): Siemens Energy reported strong revenue growth in FY2024 with Siemens Gamesa contributing significantly to offshore business revenue.

- Market share & global presence: Major market share in Europe’s offshore turbine supply and substantial presence in global project pipelines.

5) Doosan Heavy Industries and Construction (Doosan / Doosan Enerbility)

- Specialization: Engineering, procurement and construction (EPC) for power and heavy industrial projects, including offshore foundations, substations and O&M services; supply of heavy equipment and balance-of-plant.

- Key focus areas: Foundations, substations, marine construction support, turbines partnership for equipment delivery.

- Notable features: Doosan’s heavy-equipment and EPC expertise make it an important supplier/partner on large offshore projects, especially in Korea and Asia more broadly.

- 2024 revenue (company context): Doosan’s 2024 financial disclosures show multibillion KRW order and revenue figures across industrial divisions.

- Market share & global presence: Strong in Korean and Asian supply chains; participates in international EPC and foundation contracts.

Leading trends and their impact

- Larger turbines & higher capacity machines: Turbines in the 10–20+ MW class raise energy yield per unit, lowering levelized cost of energy (LCOE). This trend compresses balance-of-plant costs per MW and makes remote or low-capacity-factor sites economically viable.

- Floating offshore wind: Opens deep-water sites (e.g., off Japan, West coast U.S., Atlantic margins) and enables countries without shallow continental shelves to participate. Impact: new platforms and mooring solutions, different supply chains and risk profiles; higher CAPEX today but strong long-term potential.

- Supply-chain localization and port investments: Governments and developers are investing in port and manufacturing capacity to reduce cost and create domestic jobs. Short-term cost increases but long-term industrial benefits.

- Grid integration and hybrid projects: Co-locating offshore wind with grid reinforcements, subsea interconnectors and battery storage or hydrogen electrolyzers changes project economics and planning.

- Project finance & merchant risk management: Rising interest rates and project cost inflation have reintroduced caution; governments have re-tuned subsidy mechanisms (auctions, Contracts for Difference).

- Regional policy shifts & geopolitical risk: National energy security agendas and trade policy (local-content rules) influence where projects can be sited and who builds them.

Successful examples around the world

- Hornsea (UK, Ørsted): A multi-phased project in the North Sea that became one of the world’s largest offshore arrays (Hornsea 1 & 2 together exceed ~2.6 GW).

- Vineyard Wind 1 (U.S.): The first large-scale commercial offshore wind farm in the U.S. (approx. 806 MW), which achieved first power in 2024 using GE Haliade turbines.

- East Anglia TWO (UK, ScottishPower / Siemens Gamesa contract): Large procurement of Siemens Gamesa 14-236 DD turbines, illustrating the role of vendor project wins and supply-chain manufacturing.

- China coastal rollout: Rapid coastal installations and ambitious provincial programs (e.g., Guangdong) showcase how national industrial strategy and port investment can accelerate deployments at scale.

Global regional analysis — government initiatives & policies shaping the market

Europe (UK, Netherlands, Denmark, Germany)

Europe remains the most mature offshore market. The UK has been most aggressive — setting multi-GW targets and streamlining consenting to quadruple offshore capacity by 2030. The Crown Estate and UK government have mobilized funds for ports and supply chains. Europe also faces cost and supply-chain pressures that have led to selective subsidy increases and project re-scoping.

China & Asia

China is rapidly expanding both near-shore and deeper offshore capacity, driven by provincial targets and central planning. The 14th Five-Year Plan and provincial programs envisage tens to hundreds of GW over the coming decades, supporting domestic turbine manufacturers and heavy industry.

North America (U.S. & Canada)

The U.S. saw major policy and permitting focus in 2023–2024 to enable its first large-scale commercial projects (Vineyard Wind, Revolution Wind). Federal and state policy (permits, leasing, ports grants) and tax and incentive structures play a central role. Financing and supply-chain localization are key policy levers.

Australia & Emerging Markets

Australia and some emerging markets have pursued auctions and planning frameworks, but projects have encountered cost, regulatory and investment challenges. Some auctions have been delayed as markets recalibrate. Policymakers are balancing environmental approvals, grid planning and commercial viability.

Policy tools shaping markets

- Auctions & Contracts for Difference (CfDs): Provide revenue certainty and are widely used in Europe and being adapted elsewhere.

- Port & supply investments: Direct public or quasi-public investments reduce project CAPEX by improving logistics and local manufacturing.

- Local content rules and industrial strategy: Stimulate domestic jobs and manufacturing but can complicate international supply chains.

- Streamlined consenting and environmental frameworks: Faster permitting shortens project timelines and reduces holding costs.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Hydrogen Buses Market Revenue, Global Presence, and Strategic Insights by 2034