Table of Contents

ToggleAI-RAN Market Overview

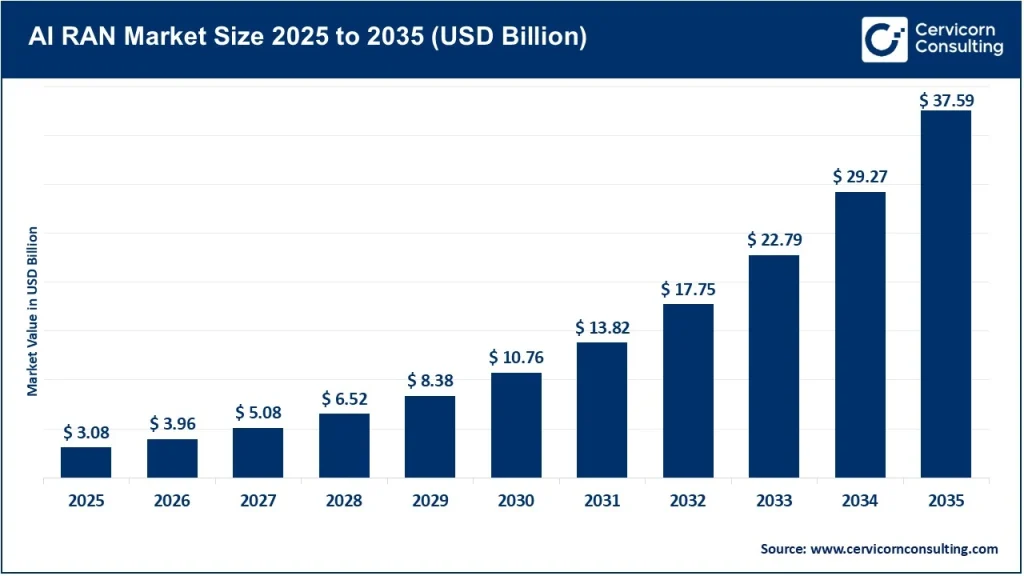

The AI-RAN market is one of the fastest-growing segments in the telecom infrastructure industry. It is projected to expand from approximately USD 3.08 billion in 2025 to nearly USD 37.59 billion by 2035 with a CAGR of 28.5%, driven by rapid digital transformation in telecom networks. North America currently leads the market, while Asia-Pacific is expected to grow at the fastest rate due to massive 5G deployments in China, India, South Korea, and Japan.

The market is segmented by:

- Component: Software, Hardware, Services

- Architecture: Open RAN, vRAN, Hybrid RAN

- Deployment: Cloud-based, On-premises

- End Users: Telecom operators, enterprises, government

What is the AI-RAN Market?

The AI-RAN (Artificial Intelligence Radio Access Network) market refers to the ecosystem where artificial intelligence is integrated into Radio Access Network (RAN) infrastructure to enhance the performance, efficiency, automation, and intelligence of mobile communication networks. Traditional RAN systems rely heavily on static configurations and manual optimization, whereas AI-RAN introduces machine learning, predictive analytics, and real-time automation to dynamically manage network traffic, energy consumption, and resource allocation.

AI-RAN represents the convergence of telecom infrastructure and AI-driven computing, enabling networks to self-optimize, self-heal, and adapt to changing traffic conditions. It plays a central role in next-generation connectivity frameworks such as 5G Advanced, edge computing, and emerging 6G architectures. The global AI-RAN market is rapidly evolving as telecom operators shift toward cloud-native, virtualized, and Open RAN-based architectures enhanced with AI capabilities.

Why is AI-RAN Important?

AI-RAN is critical because modern mobile networks are becoming increasingly complex due to exponential data growth, ultra-low latency requirements, IoT expansion, and AI-powered applications. Traditional RAN systems struggle to efficiently manage such dynamic environments.

AI-RAN addresses these challenges by:

- Enabling real-time network optimization

- Reducing operational costs through automation

- Improving energy efficiency in telecom infrastructure

- Supporting massive IoT and edge AI deployments

- Enhancing user experience through predictive traffic management

- Facilitating autonomous self-healing networks

It also enables telecom operators to transition from hardware-heavy infrastructure to software-defined and cloud-based systems, significantly improving scalability and flexibility.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2937

AI-RAN Market Growth Factors

The AI-RAN market is experiencing rapid expansion due to the increasing deployment of 5G and upcoming 6G networks, rising demand for ultra-low latency applications such as autonomous vehicles and AR/VR, growing adoption of Open RAN (O-RAN) architectures, and the shift toward cloud-native telecom infrastructure.

Additionally, the surge in AI workloads at the network edge, expansion of IoT ecosystems, rising need for energy-efficient networks, and increasing investments by telecom operators in AI-driven automation are significantly driving market growth. Strategic collaborations between telecom vendors and AI chipmakers, along with government initiatives promoting digital infrastructure modernization and smart connectivity, further accelerate adoption. The global AI-RAN market was valued at around USD 2.96–3.08 billion in 2025 and is projected to reach over USD 37 billion by 2035, growing at a CAGR of nearly 28%.

Key Companies in the AI-RAN Market

1. Nokia

- Specialization: Open RAN, AI-driven network automation, cloud-native RAN

- Key Focus Areas: AI-powered RAN optimization, 5G/6G transition, edge computing

- Notable Features: Strong focus on modular “anyRAN” architecture and AI-driven network intelligence

- 2024 Revenue (approx.): ~€22–24 billion (network infrastructure-heavy)

- Market Share: ~15–18% in global RAN ecosystem (approx.)

- Global Presence: Strong presence in Europe, North America, India, and Asia-Pacific

Nokia is increasingly positioning itself as an AI-native telecom infrastructure provider, integrating AI into optical, IP, and mobile networks.

2. Ericsson

- Specialization: 5G RAN, AI-first network automation, Open RAN solutions

- Key Focus Areas: AI-driven radio optimization, energy efficiency, network slicing

- Notable Features: AI-first RAN portfolio and strong operator partnerships

- 2024 Revenue (approx.): ~SEK 270–280 billion range (est.)

- Market Share: ~20–25% global RAN leadership

- Global Presence: Strong in North America and Europe

Ericsson is actively shifting toward AI-powered autonomous networks, although rising AI chip costs are impacting short-term margins.

3. Huawei

- Specialization: End-to-end telecom infrastructure, AI-native RAN systems

- Key Focus Areas: 5G base stations, AI-powered network intelligence, cloud RAN

- Notable Features: Highly integrated hardware-software ecosystem

- 2024 Revenue (approx.): ~$100+ billion group revenue (telecom significant portion)

- Market Share: Global leader (~30%+ in RAN equipment)

- Global Presence: Dominant in China, Asia, Middle East, Africa

Huawei leads in AI-RAN integration through its vertically integrated telecom stack and large-scale deployments.

4. Samsung Electronics

- Specialization: Virtualized RAN (vRAN), Open RAN solutions

- Key Focus Areas: Cloud-native RAN, AI optimization, private 5G networks

- Notable Features: Strong partnerships with US operators

- 2024 Revenue (approx.): ~$200+ billion total (network division smaller share)

- Market Share: ~10–15% in global RAN

- Global Presence: South Korea, US, Europe, India

Samsung is expanding aggressively in Open RAN and AI-driven virtualization for telecom networks.

5. Qualcomm

- Specialization: AI chipsets, edge computing, RAN processors

- Key Focus Areas: AI accelerators, 5G/6G modem chipsets, edge AI integration

- Notable Features: Strong semiconductor dominance in AI inference at edge

- 2024 Revenue (approx.): ~$35–40 billion

- Market Share: Dominant in mobile AI chipsets (~40–50% in mobile SoCs segment)

- Global Presence: US, Asia, Europe

Qualcomm plays a crucial enabling role in AI-RAN by providing AI-capable processors and edge computing chips.

Leading Trends in AI-RAN Market and Their Impact

- Shift to Open RAN (O-RAN):

Telecom operators are adopting vendor-neutral architectures, enabling flexibility, cost reduction, and faster AI integration. - AI-Driven Network Automation:

Networks are becoming self-optimizing and self-healing, reducing operational complexity and downtime. - Edge AI Expansion:

AI processing is moving closer to users at base stations to reduce latency and improve real-time responsiveness. - Energy-Efficient Networks:

AI is being used to dynamically manage energy consumption, reducing telecom carbon footprint. - Cloud-Native RAN Transformation:

Traditional hardware-based systems are being replaced by software-defined infrastructure. - AI + 6G Development:

Early research into 6G is heavily centered around AI-native network architecture.

Impact: These trends are transforming telecom from static infrastructure providers into intelligent digital ecosystem enablers.

Successful AI-RAN Use Cases Worldwide

- T-Mobile (USA):

Uses AI-powered RAN optimization for traffic balancing and real-time congestion management. - Vodafone (Europe):

Deploying AI-based Open RAN pilots for energy optimization and network slicing. - China Mobile:

Large-scale AI-RAN deployments integrating predictive analytics for urban network management. - NTT DoCoMo (Japan):

Uses AI-driven automation for network fault prediction and self-healing capabilities. - South Korea 5G Smart Cities:

AI-RAN is used in smart traffic systems, surveillance, and IoT-enabled urban infrastructure.

These deployments demonstrate how AI-RAN is moving from pilot projects to large-scale commercial adoption.

Global Regional Analysis & Government Initiatives

North America

- Largest market share (~37%)

- Strong presence of telecom giants and AI chipmakers

- US government promotes AI-driven 5G modernization programs

- Heavy investment in Open RAN and edge computing

Europe

- Focus on sustainability and energy-efficient telecom networks

- EU-backed funding for 6G and AI-powered telecom infrastructure

- Strong adoption of Open RAN standards

- Countries like Germany, UK, and Finland leading innovation

Asia-Pacific

- Fastest-growing region

- China, India, South Korea, and Japan driving 5G expansion

- Government subsidies for smart cities and digital infrastructure

- Massive deployment of AI-enabled telecom networks

Middle East & Africa

- Emerging adoption driven by smart city initiatives (UAE, Saudi Arabia)

- Investments in AI-based telecom modernization

Latin America

- Gradual adoption focusing on urban connectivity improvements

- Government-backed digital transformation programs

Government Policies Shaping AI-RAN Growth

- United States:

National 5G Strategy includes funding for Open RAN and AI-based telecom innovation. - European Union:

Horizon Europe and 6G research initiatives promote AI-integrated telecom infrastructure. - China:

Strong state-backed investments in AI + 5G integration for smart cities. - India:

Digital India initiative encourages AI-driven telecom modernization and 5G expansion. - Japan & South Korea:

Focus on AI-powered smart infrastructure and 6G leadership.

Final Insight

The AI-RAN market is rapidly transforming global telecommunications by merging artificial intelligence with radio access infrastructure. It is enabling networks that are not only faster and more efficient but also intelligent, autonomous, and adaptive. With strong investments from leading telecom companies, semiconductor firms, and governments worldwide, AI-RAN is positioned to become the backbone of next-generation digital connectivity, shaping the future of 5G, edge computing, and 6G ecosystems.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Microbiology Testing Market Revenue, Trends, and Strategic Insights by 2035