Distributed Cloud Market Size

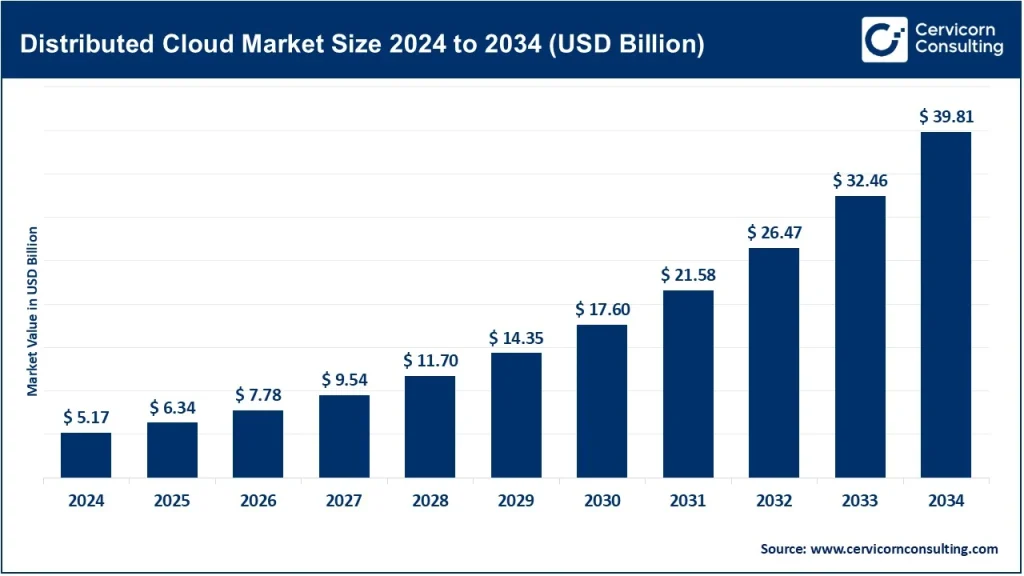

The global distributed cloud market size was worth USD 5.17 billion in 2025 and is anticipated to expand to around USD 39.81 billion by 2035, registering a compound annual growth rate (CAGR) of 22.6% from 2026 to 2035.

What Is the Distributed Cloud Market?

The distributed cloud market refers to a cloud computing model in which cloud services—such as computing, storage, networking, analytics, and AI—are delivered across multiple geographically dispersed locations while being centrally managed by a single cloud provider. Unlike traditional centralized cloud models, where workloads are hosted in a limited number of hyperscale data centers, distributed cloud enables workloads to operate closer to end users, devices, or data sources. These locations can include on-premises enterprise data centers, edge facilities, telecom infrastructure, or regional cloud nodes.

Distributed cloud combines the scalability and elasticity of public cloud platforms with the performance advantages of edge computing and the control of private cloud environments. It allows organizations to deploy applications wherever they make the most sense—whether for latency reduction, regulatory compliance, resilience, or cost optimization—while maintaining consistent security policies, governance, and operational visibility across all environments.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2850

Distributed Cloud Market Growth Factors

The distributed cloud market is expanding rapidly due to a convergence of technological, regulatory, and enterprise transformation drivers. One of the most significant growth factors is the increasing demand for data sovereignty and regulatory compliance, as governments and industry regulators require sensitive data to remain within national or regional boundaries. Enterprises are also increasingly adopting hybrid and multi-cloud strategies to improve flexibility, reduce vendor lock-in, and optimize workload placement, which naturally accelerates demand for distributed cloud architectures. The global rollout of 5G networks and improvements in high-speed connectivity further support distributed deployments by enabling ultra-low-latency processing at the network edge.

Additionally, the explosion of IoT devices, AI workloads, and real-time analytics has created massive volumes of data that are impractical to process centrally, pushing organizations to deploy computing resources closer to the data source. Together, these factors—along with ongoing digital transformation initiatives across industries—are driving sustained growth in the distributed cloud market worldwide.

Why the Distributed Cloud Market Is Important

The importance of the distributed cloud market lies in its ability to address the limitations of traditional centralized cloud infrastructure. By enabling computing and data processing closer to end users and devices, distributed cloud significantly reduces latency and improves application performance, which is critical for real-time use cases such as autonomous systems, smart manufacturing, online gaming, and financial trading platforms.

Distributed cloud is also essential for compliance with regional and industry-specific regulations, particularly in sectors such as healthcare, banking, government, and telecommunications, where data residency and privacy requirements are strict. It enables organizations to meet these requirements without sacrificing the scalability, automation, and innovation benefits of cloud computing.

Furthermore, distributed cloud enhances business resilience and reliability by reducing dependency on single centralized locations. Workloads can be dynamically shifted across locations to improve uptime and disaster recovery. As enterprises increasingly rely on AI, machine learning, and data-driven decision-making, distributed cloud provides the infrastructure foundation necessary to process data efficiently, securely, and at scale.

Key Companies in the Distributed Cloud Market

Amazon Web Services (AWS)

- Specialization: Public cloud infrastructure with distributed and edge extensions

- Key Focus Areas: Edge computing, hybrid cloud, low-latency workloads, AI and IoT integration

- Notable Features: AWS offers distributed cloud capabilities through services such as AWS Outposts, Local Zones, and Wavelength. These solutions allow customers to run AWS infrastructure and services in on-premises environments, metropolitan areas, and telecom edge locations while maintaining centralized management and security.

- 2024 Revenue / Market Share: AWS remains the global market leader in cloud services and holds the largest share of the distributed cloud market, estimated at around one-third of total market share.

- Global Presence: AWS operates a vast global infrastructure with regions, availability zones, and edge locations across North America, Europe, Asia Pacific, Latin America, and the Middle East.

Microsoft Corporation

- Specialization: Hybrid cloud and enterprise-centric distributed cloud solutions

- Key Focus Areas: Hybrid IT, edge computing, compliance-driven workloads, enterprise applications

- Notable Features: Microsoft’s distributed cloud strategy is built around Azure Arc, Azure Stack, and Azure Edge Zones, enabling seamless deployment and management of workloads across on-premises, multi-cloud, and edge environments. Strong integration with Microsoft’s enterprise software ecosystem provides a competitive advantage.

- 2024 Revenue / Market Share: Microsoft holds a significant share of the distributed cloud market, estimated at over 20%, driven by strong enterprise adoption and public sector contracts.

- Global Presence: Azure operates data centers and edge infrastructure across more than 60 regions worldwide, with strong penetration in government and regulated industries.

Cisco Systems Inc.

- Specialization: Networking-centric distributed cloud and edge infrastructure

- Key Focus Areas: Secure networking, cloud connectivity, edge orchestration, hybrid IT

- Notable Features: Cisco focuses on enabling distributed cloud environments through advanced networking, software-defined infrastructure, security, and observability platforms. Its solutions are widely used to connect and secure distributed workloads across enterprise and service-provider networks.

- 2024 Revenue / Market Share: Cisco does not disclose distributed cloud revenue separately, but it remains a major infrastructure and networking provider supporting distributed cloud deployments globally.

- Global Presence: Cisco has a strong global footprint across North America, Europe, Asia Pacific, and emerging markets.

IBM Corporation

- Specialization: Hybrid and enterprise distributed cloud solutions

- Key Focus Areas: Regulated industries, hybrid cloud modernization, AI-driven enterprise workloads

- Notable Features: IBM Cloud Satellite extends IBM Cloud services to customer-controlled environments, including on-premises and edge locations. IBM’s strength lies in compliance-focused, mission-critical workloads for industries such as finance, healthcare, and government.

- 2024 Revenue / Market Share: IBM remains a key player in enterprise distributed cloud deployments, particularly in hybrid cloud transformation initiatives.

- Global Presence: IBM operates globally with strong enterprise and government customer bases across developed and emerging markets.

Hewlett Packard Enterprise (HPE)

- Specialization: Edge-to-cloud and hybrid cloud infrastructure

- Key Focus Areas: Private cloud, edge computing, AI workloads, enterprise modernization

- Notable Features: HPE GreenLake provides a cloud-like experience for on-premises and edge environments, enabling customers to deploy and manage distributed workloads with flexible consumption models.

- 2024 Revenue / Market Share: HPE generates tens of billions of dollars in annual revenue across enterprise infrastructure, with distributed cloud forming a growing component of its hybrid cloud portfolio.

- Global Presence: HPE has a strong global presence with enterprise customers across manufacturing, telecom, government, and financial services sectors.

Leading Trends and Their Impact on the Distributed Cloud Market

Edge Computing Integration

Edge computing is becoming a core component of distributed cloud architectures. By processing data near its source, organizations can achieve faster response times and reduce bandwidth costs.

Impact: This trend is expanding distributed cloud adoption across industries such as manufacturing, transportation, energy, and smart cities.

Hybrid and Multi-Cloud Expansion

Enterprises increasingly deploy workloads across multiple cloud environments to optimize cost, performance, and risk.

Impact: Distributed cloud platforms that provide unified management across hybrid and multi-cloud environments are becoming essential for large organizations.

AI, Machine Learning, and IoT Workloads

AI and IoT applications generate massive amounts of real-time data that must be processed quickly and locally.

Impact: Distributed cloud enables scalable AI inference and analytics at the edge, accelerating adoption in sectors such as healthcare diagnostics, industrial automation, and retail personalization.

Data Sovereignty and Regulatory Compliance

Data localization laws are strengthening worldwide, especially in Europe and Asia.

Impact: Distributed cloud allows organizations to comply with regulations while maintaining centralized cloud operations, making it a preferred deployment model for regulated industries.

Telecom and 5G Partnerships

Cloud providers are increasingly partnering with telecom operators to deploy distributed cloud services at the network edge.

Impact: These partnerships enable ultra-low-latency applications such as autonomous vehicles, smart infrastructure, and immersive digital experiences.

Successful Examples of Distributed Cloud Adoption Worldwide

One of the most prominent examples is the deployment of cloud infrastructure at telecom edge locations, enabling low-latency services for mobile users and IoT devices. Major cloud providers have launched localized cloud zones in metropolitan areas to support gaming, media streaming, and financial trading platforms.

Large retail chains use distributed cloud architectures to process data locally in stores while synchronizing insights centrally, enabling real-time inventory management and personalized customer experiences. Manufacturing companies deploy edge-based cloud systems in factories to support predictive maintenance and automated quality control.

Financial institutions leverage distributed cloud to process transactions locally for compliance reasons while maintaining centralized risk analytics and reporting. Healthcare providers use distributed cloud platforms to store and analyze patient data within regional boundaries while enabling advanced diagnostics and telemedicine services.

Global Regional Analysis and Government Initiatives

North America

North America leads the distributed cloud market due to early cloud adoption, advanced digital infrastructure, and strong investments from hyperscale providers. Government initiatives promoting cloud modernization, cybersecurity, and digital public services have accelerated adoption across both public and private sectors.

Europe

Europe’s distributed cloud growth is driven by strict data protection and privacy regulations. Governments and enterprises prioritize data sovereignty, leading to widespread adoption of localized and hybrid cloud architectures. Public-private partnerships and regional digital infrastructure programs further support market growth.

Asia Pacific

Asia Pacific is the fastest-growing region in the distributed cloud market. Rapid digitalization, expanding 5G networks, and government-led cloud-first initiatives are driving adoption across countries such as China, India, Japan, South Korea, and Southeast Asia. Public sector digitization and smart city programs are major contributors.

Latin America

Latin America is experiencing steady growth as governments invest in digital transformation, cloud adoption, and improved connectivity. While the market is still emerging, distributed cloud adoption is increasing in banking, telecom, and e-government services.

Middle East and Africa

The Middle East and Africa region is gradually adopting distributed cloud technologies, supported by government-backed digital economy initiatives, smart infrastructure projects, and investments in data centers. Adoption remains uneven but is expected to accelerate as connectivity improves.

Government Initiatives and Policies Shaping the Market

Key government initiatives influencing the distributed cloud market include data localization laws, national cloud strategies, public sector cloud migration programs, cybersecurity frameworks, and investments in 5G and edge infrastructure. Policies promoting digital sovereignty, smart cities, and AI innovation continue to shape distributed cloud adoption globally.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us

Read Report: Generative AI in Healthcare Market Revenue, Global Presence, and Strategic Insights by 2034